Are Traditional 60/40 Portfolios Dead? How Accredited Investors Are Diversifying With Private Equity and Digital Assets

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Feb 11

- 5 min read

Let's settle this debate once and for all: the 60/40 portfolio isn't dead. It's just not the only game in town anymore.

For decades, the classic 60% stocks and 40% bonds split was the bedrock of portfolio construction. It was simple, effective, and made sense. Stocks gave you growth, bonds provided stability, and together they worked like a well-oiled machine.

Then 2022 happened.

The Year Everything Broke

When both stocks and bonds tanked simultaneously in 2022, losing 15.3% together, the financial media went into a frenzy. Headlines screamed that the 60/40 portfolio was finished. Dead. Obsolete. Time to throw out the old playbook.

But here's the thing about market panics: they rarely tell the whole story.

The Comeback Nobody Talks About

Fast forward to today, and the 60/40 portfolio has staged an impressive comeback. After that brutal 2022, it gained 18% in 2023, another 15.5% in 2024, and 13.6% in 2025. That's exactly what mean reversion looks like in action.

Morgan Stanley found that historically, there's an 80% probability of positive returns in the two years following a simultaneous decline in stocks and bonds. The data proved itself right again.

So why are we still talking about this? Because "not dead" doesn't mean "optimal."

The Real Problem: Forward Returns Are Underwhelming

Here's where it gets interesting. While the 60/40 survived, its expected real returns for 2026 sit around 3.4%, well below the historical average of nearly 5% since 1900.

For most retail investors, that might be acceptable. But if you're an accredited investor managing serious wealth, 3.4% real returns probably aren't going to cut it. You're looking for better risk-adjusted returns, meaningful diversification, and access to opportunities that aren't available to everyone else.

That's where the landscape starts to shift.

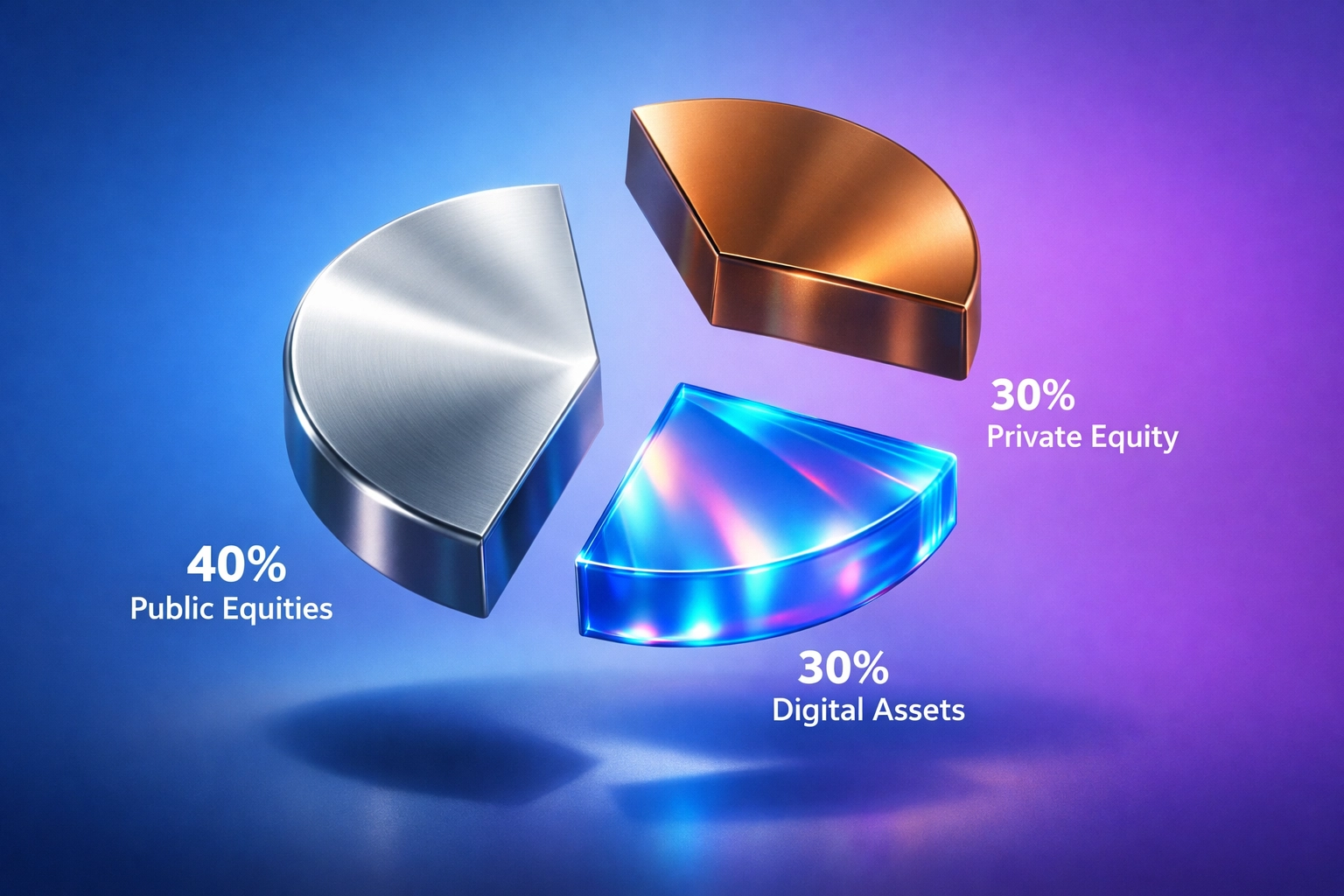

The Evolution: From 60/40 to 40/30/30

Instead of abandoning the principles that made 60/40 work, sophisticated investors are evolving them. The new model looks something like this:

40% Public Equities - Still your growth engine, but more strategic than just buying the S&P 500.

30% Private Equity & Alternatives - This is where accredited investors have a real edge. Private equity, venture capital, real estate syndications, and private credit offer returns that aren't correlated with public markets.

30% Digital Assets & Emerging Opportunities - Bitcoin, institutional-grade crypto strategies, and blockchain-based investments that provide both diversification and asymmetric upside potential.

This isn't about being trendy. It's about accessing asset classes that genuinely behave differently than stocks and bonds.

Why Private Equity Changes the Game

Private equity has consistently delivered returns that outpace public markets, often with lower volatility. The catch? It's illiquid, requires larger minimum investments, and typically has longer lock-up periods.

For accredited investors, that's not a bug: it's a feature.

The illiquidity premium is real. By committing capital for 5-10 years, you're compensated for that patience. You're also getting access to companies before they go public, when the most explosive growth typically happens.

Private equity isn't just buyouts anymore either. The landscape now includes:

Venture capital targeting early-stage tech and innovation

Growth equity in established private companies

Private credit offering fixed income with better yields than traditional bonds

Real estate syndications providing both income and appreciation

The key is having the right allocation and the right partners. A 30% allocation to private markets can dramatically improve your overall portfolio efficiency without taking on excessive risk.

The Digital Asset Question

Let's address the elephant in the room: Bitcoin and digital assets.

Five years ago, mentioning crypto in the same breath as "institutional portfolio" would get you laughed out of the room. Today? Major pension funds, endowments, and family offices are allocating to digital assets through proper institutional channels.

The difference is approach. We're not talking about speculating on meme coins or trying to time the crypto market. Institutional crypto integration means:

Bitcoin as digital gold - A finite, uncorrelated asset that acts as a hedge against monetary debasement

Structured products that provide exposure with downside protection

Staking and yield strategies through regulated custodians

Blockchain infrastructure investments rather than pure token speculation

A 5-10% allocation to institutional-grade digital assets can provide meaningful diversification benefits. Bitcoin has shown low correlation to traditional assets, and during certain market cycles, it's been one of the few things working when everything else struggled.

The critical piece is doing this through proper custodians, with clear tax reporting, and through strategies that make sense for your overall risk profile.

Risk Mitigation in the New Model

Here's what keeps me up at night: not market volatility, but concentration risk.

Traditional 60/40 portfolios are actually highly concentrated: concentrated in public markets, concentrated in developed economies, and concentrated in the same systematic risks everyone else is taking.

By spreading capital across private equity, real estate, digital assets, and traditional holdings, you're building what I call "true diversification." You're not just diversifying within public markets. You're diversifying across entirely different return drivers.

Private equity returns are driven by operational improvements and strategic positioning. Real estate is driven by tangible asset appreciation and rental yields. Bitcoin is driven by adoption and scarcity. These fundamentally different mechanisms create a more resilient portfolio.

The Access Advantage

This is where being an accredited investor really matters. The SEC's accredited investor definition isn't just regulatory gatekeeping: it acknowledges that certain opportunities require both financial resources and sophistication.

Private equity funds, hedge funds, and institutional digital asset products simply aren't available to retail investors. But for those who qualify, these opportunities can be transformative.

At Mogul Strategies, we're built around this exact premise: blending traditional asset management discipline with access to innovative strategies that most investors never see. It's not about chasing returns or following trends. It's about constructing portfolios that can weather different market environments while capturing opportunities across the full investment spectrum.

What This Means For You

If you're still running a pure 60/40 portfolio in 2026, you're not wrong: but you might be leaving returns on the table.

The evolution isn't about abandoning what works. It's about recognizing that the investment universe has expanded dramatically. Accredited investors have access to tools and opportunities that can genuinely improve outcomes.

The question isn't whether the 60/40 is dead. The question is: why limit yourself to only two asset classes when you can access five or six with meaningfully different risk and return characteristics?

Smart diversification in 2026 means going beyond stocks and bonds. It means thoughtful allocation to private markets, strategic exposure to digital assets, and working with partners who understand how to blend traditional and innovative strategies.

The 60/40 portfolio isn't dead. It's just not enough anymore.

Ready to explore how alternative investments could enhance your portfolio? Visit Mogul Strategies to learn more about our approach to modern portfolio construction for accredited investors.

Comments