Are Traditional Institutional Portfolios Dead? How Accredited Investors Are Getting 15%+ Returns with Diversified Alternatives

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Feb 2

- 5 min read

The investment world loves a dramatic headline. "The 60/40 portfolio is dead!" "Traditional investing is over!" But here's the truth: traditional institutional portfolios aren't dead, they're evolving. And the investors who understand this shift are positioning themselves for significantly better returns.

If you're an accredited investor still relying solely on stocks and bonds, you're leaving serious money on the table. Let's talk about what's actually happening and how sophisticated investors are adapting.

The Real Story Behind Traditional Portfolio Evolution

Traditional portfolios aren't dying, they're being rebuilt from the ground up. Over the past decade, major endowments and foundations have quietly shifted their equity allocations from around 52% to nearly 65%. That's not a small adjustment; it's a fundamental rethinking of risk and return.

The catalyst? A perfect storm of persistent low bond yields, maturing alternative asset classes, and the realization that the old 60/40 split just doesn't deliver the returns investors need anymore. When bonds yield 3-4% and inflation runs hot, you need a new playbook.

Recent surveys show that 65% of institutional investors now believe a portfolio with 20% alternatives will outperform traditional allocations. But here's where it gets interesting: many sophisticated investors are going much further than 20%.

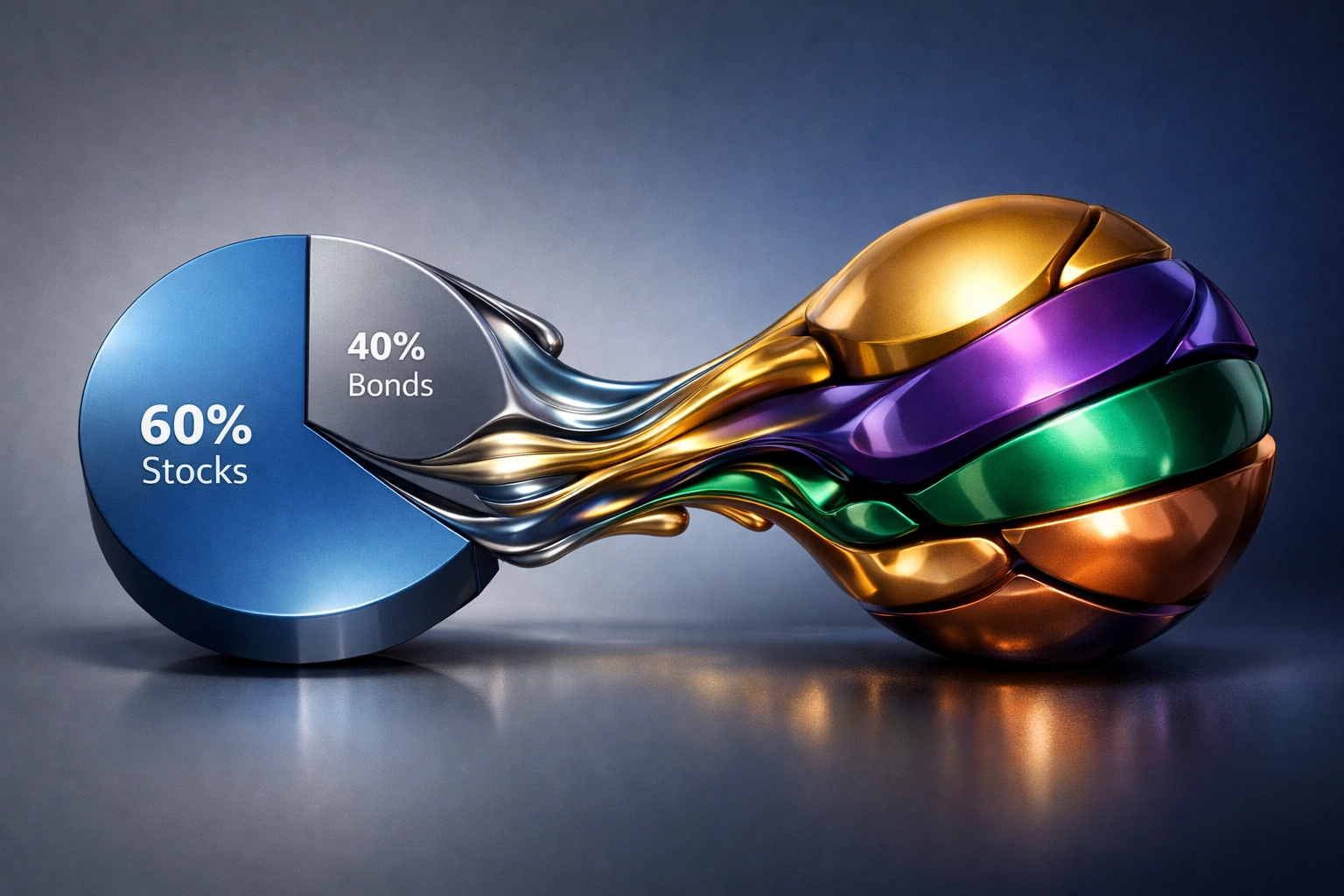

The New Diversification Model: Beyond 60/40

The traditional 60/40 portfolio (60% stocks, 40% bonds) served investors well for decades. But times have changed. Today's institutional investors are adopting models that look more like 40/30/30 or even more aggressive alternative allocations.

What does this actually mean?

40% Public Equities: Still maintaining exposure to stock market growth, but with a more selective, strategic approach.

30% Fixed Income & Cash: Providing stability and liquidity, but not betting the farm on low-yielding bonds.

30% Alternative Investments: This is where the magic happens, private equity, real estate, hedge funds, and increasingly, digital assets.

Some endowments and family offices are pushing alternative allocations even higher, to 40-50% of their portfolios. Why? Because alternatives offer something traditional assets can't: non-correlated returns and access to premium opportunities.

Breaking Down the Alternatives Opportunity

Let's get specific about where those enhanced returns are coming from.

Private Equity

Private equity has outperformed public equity by roughly 500 basis points annually over the past decade. That's not a typo, we're talking about a 5% annual premium for taking illiquidity risk and accessing companies before they go public.

For accredited investors, this means accessing venture capital, growth equity, and buyout funds that were historically reserved for large institutions. The catch? You need to be comfortable with 5-10 year lockup periods.

Private Credit

With senior-secured U.S. direct lending yielding 200-300 basis points above comparable public market alternatives, private credit has become a major portfolio component. You're essentially becoming the bank, lending directly to middle-market companies at attractive rates.

The risk is real, you're taking on credit exposure, but for accredited investors with proper due diligence, the risk-adjusted returns can be compelling.

Real Estate Syndication

Real estate has always been an institutional favorite, but the game has changed. Instead of REITs that trade on public markets, sophisticated investors are accessing real estate through syndication deals, apartment complexes, self-storage facilities, industrial properties.

The structure is straightforward: you pool capital with other accredited investors to buy properties that would be out of reach individually. Returns typically come from both cash flow and appreciation, with many deals targeting 12-18% annualized returns.

Digital Assets & Crypto Integration

Here's where things get controversial, and interesting. Institutional investors are no longer ignoring Bitcoin and crypto. Major endowments have added 1-5% allocations to digital assets, recognizing them as a legitimate alternative asset class.

The key is treating crypto like any other alternative: size it appropriately, understand the risks, and integrate it into a broader diversification strategy. A 3-5% allocation to Bitcoin can add meaningful diversification without dominating portfolio risk.

Hedge Fund Strategies

Hedge funds get a bad rap, but certain strategies offer genuine value. Market-neutral funds, managed futures, and global macro strategies can provide returns regardless of market direction, the ultimate diversification benefit.

The fee structure is higher, yes, but for investors seeking true portfolio resilience, the right hedge fund allocations can smooth out volatility while maintaining upside potential.

Let's Talk Real Numbers

Here's where we need to inject some realism. The "15%+ returns" in the headline isn't fantasy, but it's not guaranteed either.

What the data actually shows:

Well-constructed alternative portfolios have consistently delivered 8-12% annual returns over rolling 10-year periods

Top-quartile private equity funds have achieved 15-20% returns, but average funds do significantly less

Diversified alternative allocations typically target 7-10% real returns (after inflation)

The investors achieving 15%+ are typically doing several things right:

They're accessing top-tier managers (this matters more in alternatives than public markets)

They're properly diversifying across alternative strategies

They're maintaining discipline during market cycles

They're sizing positions appropriately for illiquidity

You can absolutely achieve enhanced returns through alternatives, but it requires sophistication, patience, and realistic expectations.

The Total Portfolio Approach

The smartest institutional investors have stopped thinking in traditional asset class silos. Instead, they're adopting a Total Portfolio Approach (TPA) that evaluates every investment based on its contribution to overall objectives:

Return: What's the expected return across market cycles?

Liquidity: Can you access capital when needed?

Diversification: How does this move independently from other holdings?

Resilience: How does it perform in various economic scenarios?

This framework shifts the conversation from "Should I own bonds?" to "What role does this investment play in achieving my long-term objectives?"

It's a subtle but powerful difference. Suddenly, a 10-year private equity lockup isn't scary: it's a strategic choice to capture illiquidity premium while maintaining adequate liquidity elsewhere in the portfolio.

Making the Transition

If you're an accredited investor looking to evolve your portfolio, here's the roadmap:

Start with education. Alternatives aren't more complex than they need to be, but they do require understanding. Learn the structures, fee arrangements, and risk characteristics.

Assess your liquidity needs. How much of your portfolio can be locked up for 3-10 years? Be honest: alternatives require patient capital.

Work with experienced partners. The difference between top-quartile and median alternative investments is massive. Access and due diligence matter enormously.

Build gradually. You don't need to overhaul your entire portfolio overnight. Start with 10-15% alternatives and increase as you gain comfort and experience.

The Bottom Line

Traditional institutional portfolios aren't dead: they're being rebuilt with better tools. The 60/40 portfolio was never a law of nature; it was just the best option available for a particular era.

Today's investing landscape offers accredited investors unprecedented access to alternatives that were once exclusive to large endowments. The question isn't whether to evolve your portfolio: it's how quickly you can do it intelligently.

At Mogul Strategies, we help accredited and institutional investors navigate this transition, blending traditional assets with innovative alternatives to build portfolios designed for today's reality, not yesterday's playbook.

Ready to explore how alternatives can enhance your portfolio? Let's start the conversation.

Comments