Diversified Portfolio Strategies: The 40/30/30 Model Institutional Investors Are Using in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Feb 3

- 5 min read

The investment playbook that worked for decades is getting a major rewrite. If you're still running a traditional 60/40 portfolio: 60% stocks, 40% bonds: you probably felt the pain in 2022 when both asset classes tanked together. That wake-up call sent institutional investors scrambling for a better approach, and what's emerging is the 40/30/30 model.

Let's break down what this means, why it matters, and whether it's right for your portfolio.

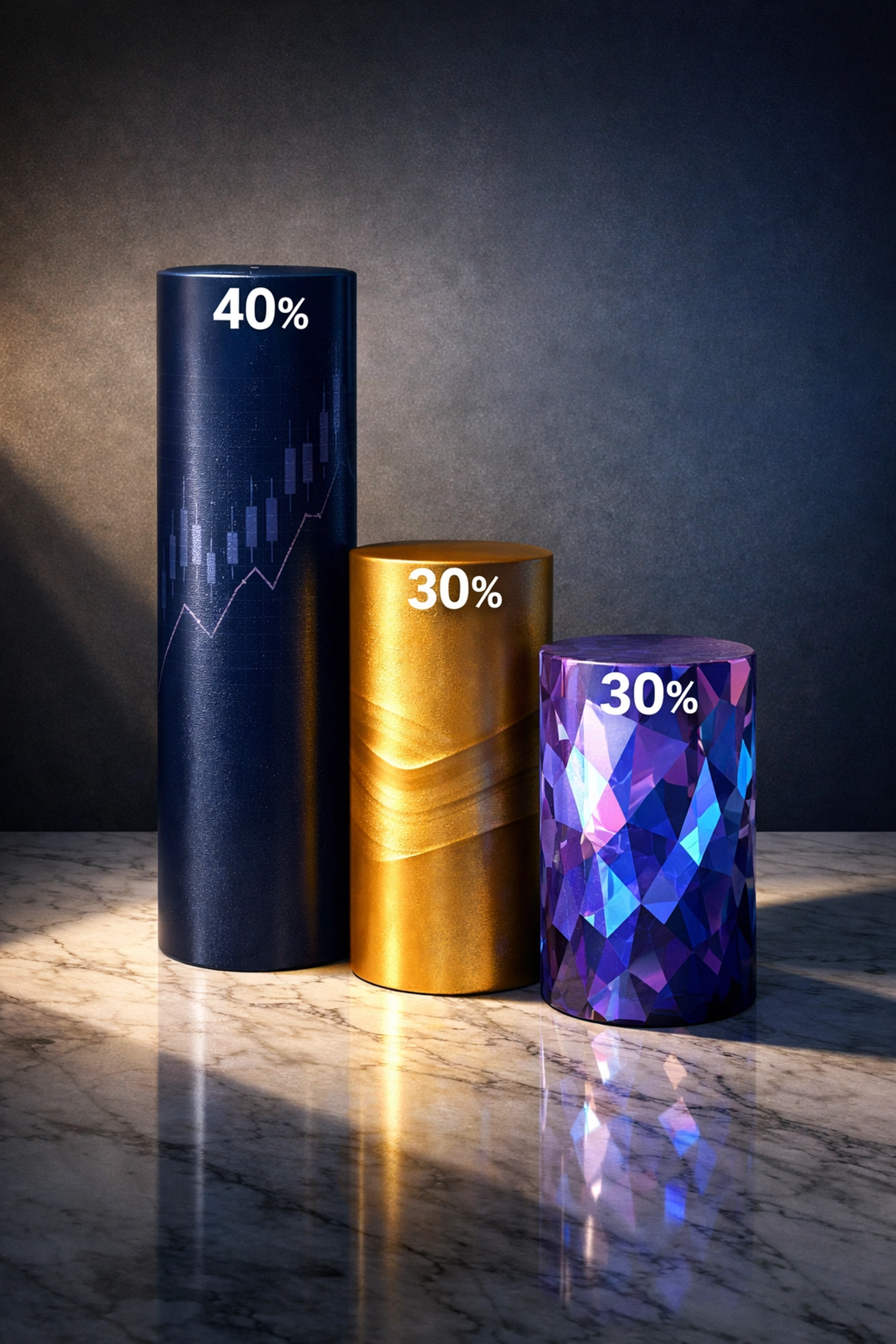

What Exactly Is the 40/30/30 Portfolio?

The math is simple: 40% public equities, 30% fixed income, and 30% alternative investments. Think of it as the 60/40 model's smarter cousin: one that learned from recent market chaos and adapted accordingly.

The big difference? That 30% slice dedicated to alternatives. We're talking about assets that don't march in lockstep with stocks and bonds: private equity, real estate, infrastructure projects, managed futures, and even commodities. The goal is to have a third pillar that zigs when the other two zag.

Why the Traditional 60/40 Is Struggling

For years, the 60/40 split was the gold standard. Stocks delivered growth, bonds provided stability and income, and when one went down, the other usually held steady. It was a beautiful relationship.

Then inflation came roaring back, central banks jacked up interest rates, and suddenly both stocks and bonds were falling together. The diversification benefit that made 60/40 so attractive just... disappeared.

We haven't seen this kind of environment since the 1980s. Interest rates that stay "higher for longer" fundamentally change how stocks and bonds behave. When rates rise, bond prices fall (that's just math), but higher rates also pressure stock valuations, especially for growth companies. The result? Your diversification fails exactly when you need it most.

2022 was the perfect example. Both stocks and bonds got hammered as inflation spiked and the Fed raised rates aggressively. Investors who thought they were diversified watched their "safe" bond allocations drop alongside their equities. Not fun.

The Performance Case for 40/30/30

Here's where it gets interesting. If you look purely at total returns from 2001 to 2025, the 40/30/30 model actually underperformed the traditional 60/40: 6.89% annual returns versus 7.46%. So why would anyone make this switch?

Risk-adjusted returns tell a different story.

The 40/30/30 portfolio posted a Sharpe ratio of 0.71 compared to 0.56 for the 60/40 mix. In plain English, you're getting better returns for the level of risk you're taking on. That's what institutional investors care about: not just making money, but making it efficiently.

More importantly, the diversification benefit showed up during market stress events: the dot-com crash, the 2008 financial crisis, the COVID-19 panic in 2020, and that brutal 2022 bear market. When things got ugly, the alternatives cushioned the blow.

Research from J.P. Morgan found that adding a 25% allocation to alternatives can boost 60/40 returns by 60 basis points: that's an 8.5% improvement on a projected 7% return. KKR's analysis showed that 40/30/30 outperformed 60/40 across all time periods they studied.

What Goes Into the Alternatives Bucket?

This is where strategy gets personal, but the 30% alternatives allocation typically includes:

Private Equity – Investments in companies that aren't publicly traded. Higher potential returns, but you're locked in for years.

Real Assets – Infrastructure projects like toll roads, utilities, or cell towers. Real estate investment trusts (both public and private). Commodities that hedge against inflation.

Managed Futures – Systematic trading strategies that can profit in both rising and falling markets.

Credit Instruments – High-yield bonds, private credit, and other fixed-income alternatives that offer different risk-return profiles than traditional bonds.

The beauty of real assets like infrastructure and real estate is that many of these investments have inflation adjustments built directly into their contracts. When inflation rises, your cash flows increase automatically. That's a genuine hedge, not just theory.

The Implementation Reality Check

Here's the truth: building a proper 40/30/30 portfolio isn't as simple as rebalancing your brokerage account.

For institutional investors, this model makes a lot of sense. You have access to private equity funds, institutional real estate deals, and infrastructure investments that retail investors simply can't touch. You can afford the higher fees that come with alternative investments because you're investing serious capital. And you have the sophistication to evaluate complex investment structures.

For accredited investors, you're in a middle ground. You can access some private alternatives through feeder funds or specialized vehicles, but you'll pay for the privilege. The minimum investments might be steep: think $100,000 to $250,000 per position. You need to understand illiquidity risk because private alternatives often lock up your money for 5-10 years.

For retail investors, implementing a true 40/30/30 is challenging but not impossible. You can use publicly traded alternatives like REITs, commodity ETFs, and liquid alternative mutual funds. The tradeoff is that these public versions often have higher correlation to traditional assets than their private counterparts. You might get 60-70% of the diversification benefit at best.

The Tradeoffs Nobody Talks About

Let's be honest about the downsides:

Higher fees. Alternative investments aren't cheap. Private equity funds often charge 2% management fees plus 20% of profits. Real estate syndications might charge 1-2% annually plus acquisition fees. These costs eat into returns.

Complexity. Managing three distinct asset classes with different liquidity profiles, tax treatments, and reporting requirements is way more complicated than rebalancing between two index funds.

Bull market underperformance. During raging bull markets when stocks are up 20-30%, your 40/30/30 portfolio will lag behind. That 30% in alternatives might return 8-12% while your friends with 60% in stocks are crushing it. You need the discipline to stick with the strategy.

False diversification. Not all alternatives actually diversify. Some marketed "alternative" investments: like high-yield bonds: have significant equity market correlation. They'll still drop when stocks crash. Due diligence matters.

Making It Work in 2026 and Beyond

The 40/30/30 model isn't a magic formula, but it represents an evolution in thinking about portfolio construction. The key insight is that traditional diversification between stocks and bonds isn't enough in today's market environment.

At Mogul Strategies, we help investors navigate this shift by blending traditional asset management with innovative strategies. Whether that's identifying institutional-grade private opportunities, integrating digital assets thoughtfully, or structuring real estate investments with proper diversification: the goal is building resilient portfolios that can weather whatever markets throw at them.

The bottom line? If 2022 taught us anything, it's that the old rules of diversification need updating. The 40/30/30 model won't eliminate losses during downturns, but it's designed to reduce the severity and recover faster. For institutional and accredited investors with the access and capital to implement it properly, that's a compelling value proposition.

Just make sure you understand what you're buying in that alternatives bucket. Not all diversification is created equal.

Comments