The 40/30/30 Framework: A Proven Diversified Portfolio Strategy for Accredited Investors

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 25

- 5 min read

If you've been investing for any length of time, you've probably heard of the classic 60/40 portfolio. Sixty percent stocks, forty percent bonds. Simple, balanced, and for decades: pretty effective.

But here's the thing: markets have changed. And if 2022 taught us anything, it's that the old playbook doesn't always work the way it used to.

That year, both stocks and bonds dropped together. The diversification benefit that 60/40 was supposed to provide? It vanished when investors needed it most. Rising inflation and aggressive interest rate hikes created a perfect storm that exposed a fundamental vulnerability in traditional portfolio construction.

Enter the 40/30/30 framework: a modern approach that's gaining serious traction among institutional investors and accredited individuals looking for better risk-adjusted returns.

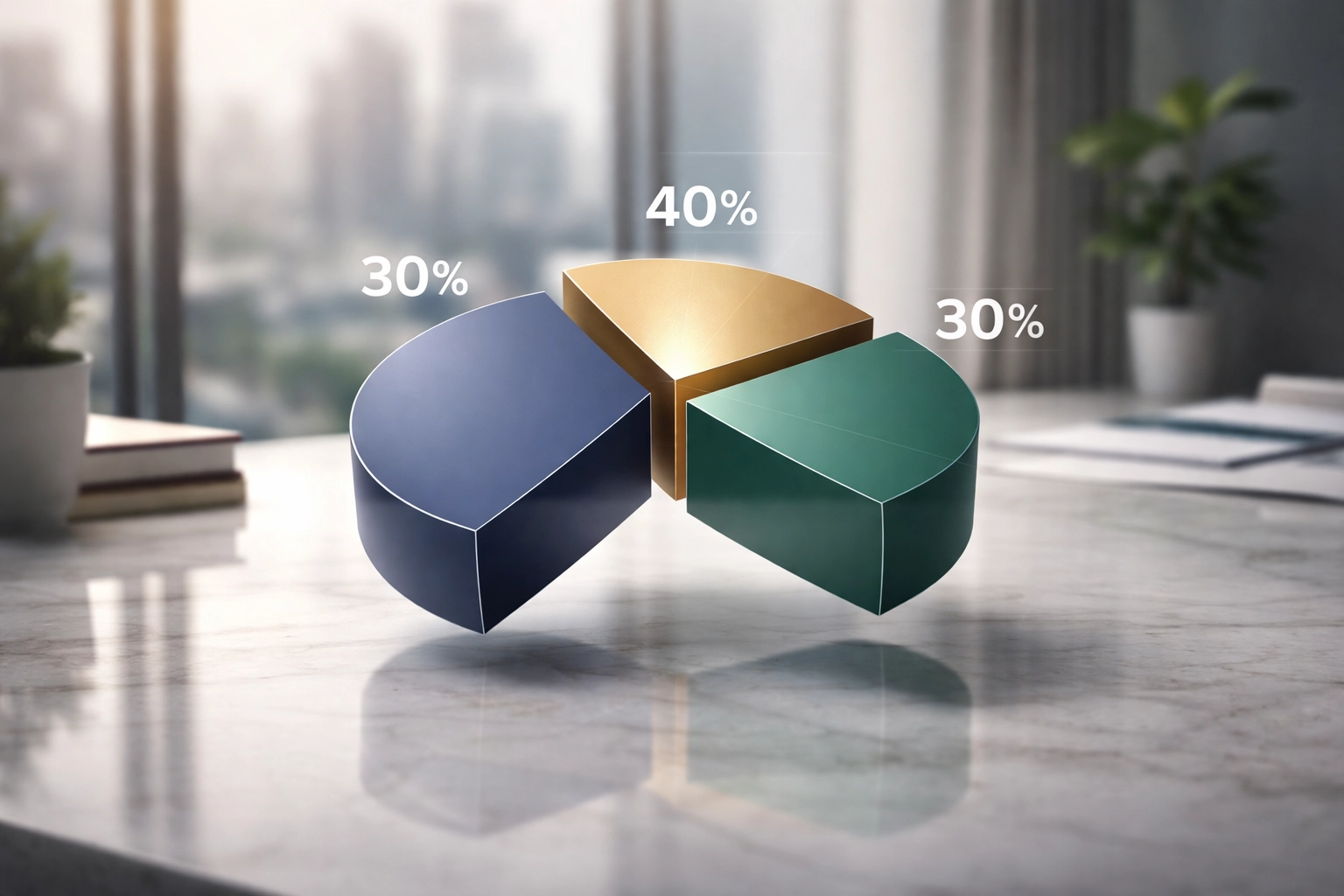

What Exactly Is the 40/30/30 Framework?

Let's break it down:

40% Public Equities – Your stocks, index funds, and equity exposure

30% Fixed Income – Bonds, treasuries, and other debt instruments

30% Alternative Investments – This is where it gets interesting

The framework essentially takes 20% from your equity allocation and 10% from your bond allocation, then redirects that capital into alternatives. It's not a radical departure from traditional investing: it's an evolution of it.

The goal? Create a portfolio that doesn't move in lockstep with traditional markets. When stocks and bonds zig together (like they did in 2022), you want something in your portfolio that zags.

Why Alternatives Matter More Than Ever

Here's a question: Why did institutional investors: pension funds, endowments, family offices: embrace alternatives decades ago while most individual investors stuck with stocks and bonds?

The answer is access. For years, alternatives like private equity, hedge funds, and real estate syndications were simply off-limits to anyone who wasn't writing eight-figure checks.

That's changed. Accredited investors now have pathways into strategies that were once reserved for the Yale Endowment and sovereign wealth funds.

And the timing couldn't be better.

Alternative investments offer something crucial: lower correlation to traditional asset classes. When your stocks are getting hammered and your bonds aren't providing the buffer they're supposed to, alternatives can potentially smooth out the ride.

Think about it this way: infrastructure investments often have built-in inflation adjustment clauses. Real estate generates income regardless of what the S&P 500 is doing on any given Tuesday. Absolute return strategies aim to make money in any market environment.

These aren't just nice-to-haves anymore. For sophisticated investors, they're becoming essential portfolio components.

The Numbers: Performance and Risk-Adjusted Returns

Let's talk data, because at the end of the day, that's what matters.

Research from J.P. Morgan found that adding a 25% allocation to alternatives could boost 60/40 returns by approximately 60 basis points. That might not sound like much, but it represents an 8.5% improvement on the 60/40 portfolio's projected 7% annual return. Over a 20 or 30-year investment horizon, that compounds into serious wealth.

KKR's research went even further, finding that 40/30/30 outperformed 60/40 across all timeframes they studied.

But here's where it gets nuanced: and where honest analysis matters.

Looking at data from November 2001 through August 2025, a 40/30/30 portfolio actually produced slightly lower total returns than 60/40 (6.89% CAGR versus 7.46%). However, it significantly outperformed on a risk-adjusted basis, with a Sharpe ratio of 0.71 compared to 0.56.

What does that mean in plain English? The 40/30/30 portfolio delivered better returns per unit of risk taken. You might give up a fraction of upside during roaring bull markets, but you're positioned much better for the inevitable downturns.

For accredited investors focused on wealth preservation alongside growth: which is most of you: that trade-off often makes sense.

Building Your Alternatives Sleeve: The Three-Part Approach

Not all alternatives are created equal. Simply throwing 30% of your portfolio into "alternative stuff" isn't a strategy: it's a recipe for confusion.

The framework calls for a thoughtful three-part approach within that alternatives allocation:

1. Enhancers

These are your return amplifiers. Private equity falls into this bucket: investments designed to potentially boost overall portfolio returns above what public markets can deliver.

The trade-off? Less liquidity and longer time horizons. But for patient capital, the historical returns from quality private equity managers have been compelling.

2. Diversifiers

Think absolute return strategies and hedge funds that genuinely aim to be uncorrelated with your other holdings. The key word here is "genuinely": not every fund that calls itself uncorrelated actually delivers on that promise.

This is where manager selection becomes critical. A well-chosen diversifier can provide stability when traditional markets get volatile. A poorly chosen one just adds complexity and fees without the benefit.

3. Inflation Hedges

Assets that offer protection when inflation surprises to the upside. Real estate, infrastructure, commodities, and certain real assets fall into this category.

These investments often have contractual mechanisms (like inflation-adjusted lease agreements) that help maintain purchasing power during inflationary periods: exactly when traditional bonds tend to struggle.

What Actually Goes in That 30%?

Let's get specific. For accredited investors, the alternatives sleeve might include:

Private Equity – Access to companies before they go public, or buyouts of established private businesses. Higher return potential, but requires longer holding periods.

Real Estate Syndications – Pooled investments in commercial properties, multifamily developments, or specialized real estate sectors. Offers income and appreciation potential outside public markets.

Hedge Fund Strategies – Long/short equity, global macro, or market-neutral approaches. The best managers aim to generate returns regardless of market direction.

Digital Assets – For forward-thinking portfolios, institutional-grade Bitcoin and crypto exposure is becoming a legitimate consideration. This isn't about speculation: it's about adding an asset class with historically low correlation to traditional investments.

Infrastructure – Investments in essential assets like utilities, transportation, and energy. Often provides steady income with built-in inflation protection.

The specific mix depends on your goals, risk tolerance, and time horizon. There's no one-size-fits-all allocation within the alternatives sleeve.

Important Considerations

Let's be real about the challenges.

Higher fees – Alternatives typically cost more than index funds. You're paying for active management, specialized expertise, and access to opportunities unavailable in public markets.

Complexity – These aren't set-it-and-forget-it investments. Due diligence matters, and ongoing monitoring is essential.

Liquidity constraints – Many alternatives lock up your capital for extended periods. You need to plan accordingly.

Manager selection – The dispersion of returns in alternatives is much wider than in traditional asset classes. The difference between a top-quartile and bottom-quartile private equity manager can be enormous. Picking the right partners matters immensely.

This is precisely why working with experienced advisors who specialize in alternative investments makes such a difference. The potential benefits are real, but so are the pitfalls of poor implementation.

The Bottom Line

The 40/30/30 framework isn't about chasing returns or following the latest trend. It's about building a portfolio designed for the market environment we actually live in: one where traditional diversification sometimes fails, where inflation can spike unexpectedly, and where correlation between asset classes doesn't always behave the way textbooks suggest.

For accredited investors serious about long-term wealth preservation and growth, dedicating meaningful portfolio allocation to alternatives isn't optional anymore. It's becoming standard practice.

The question isn't whether alternatives belong in your portfolio. It's how to implement them thoughtfully: with the right partners, the right strategies, and the right expectations.

At Mogul Strategies, we specialize in helping accredited investors navigate exactly these decisions. Whether you're exploring your first alternatives allocation or looking to optimize an existing portfolio, the 40/30/30 framework offers a proven starting point for the conversation.

Comments