The 40/30/30 Model Explained: A Smarter Approach to Diversified Portfolio Strategies

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 18

- 5 min read

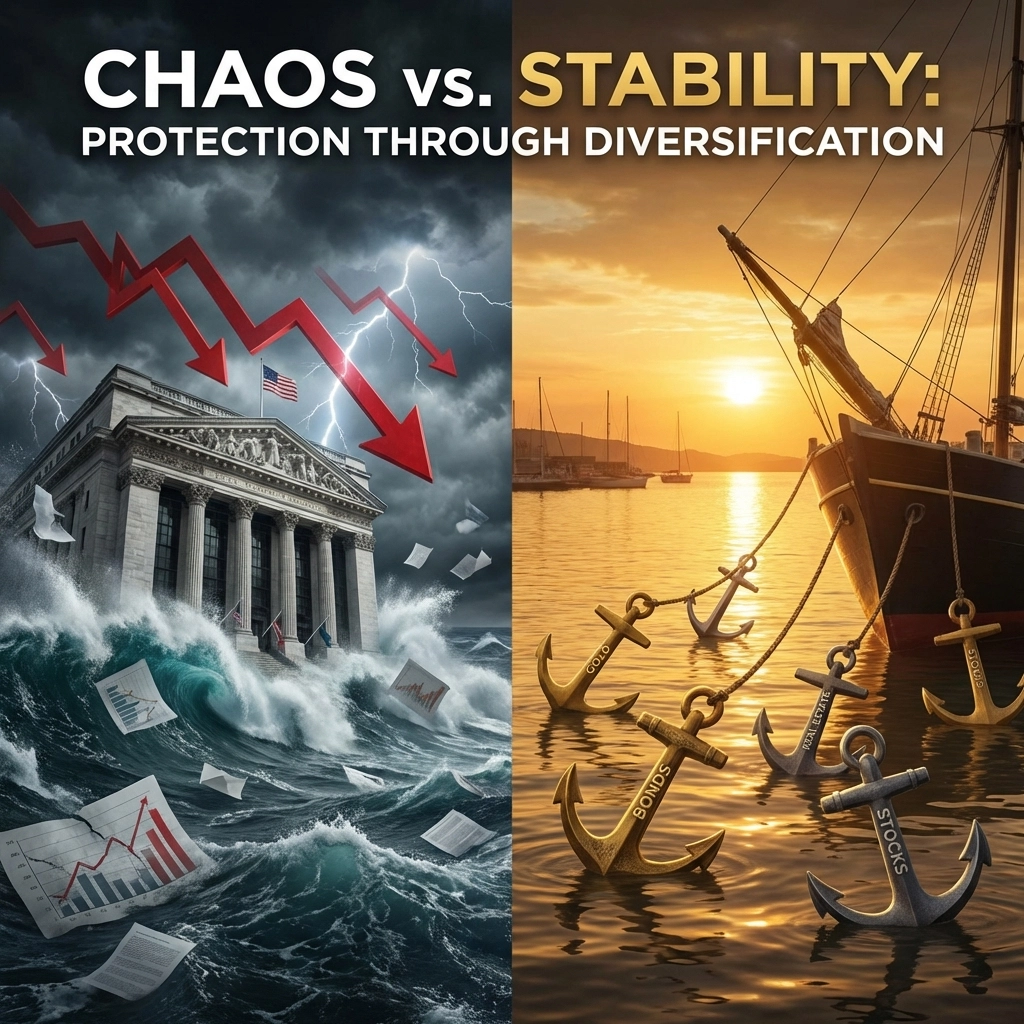

If you've been in the investment world for any length of time, you've probably heard of the classic 60/40 portfolio. It's been the go-to framework for decades: 60% stocks, 40% bonds, and call it a day.

But here's the thing, what worked beautifully for the last 40 years has started showing some serious cracks. And if 2022 taught us anything, it's that the old playbook might need a rewrite.

Enter the 40/30/30 model. It's not a revolutionary concept, but it is a smarter evolution of portfolio construction that addresses the fundamental weaknesses of traditional diversification. Let's break it down.

What Exactly Is the 40/30/30 Model?

The 40/30/30 model is a portfolio allocation framework that splits your investments into three distinct buckets:

40% Public Equities – Your stocks, ETFs, and publicly traded securities

30% Fixed Income – Bonds, treasuries, and other debt instruments

30% Alternative Assets – Real estate, private equity, infrastructure, private credit, and other non-traditional investments

The magic happens in that third bucket. By carving out a meaningful allocation to alternatives, you're introducing assets that don't move in lockstep with stocks or bonds. And that's where real diversification actually lives.

Why the 60/40 Model Isn't Cutting It Anymore

For decades, the 60/40 portfolio was considered the gold standard. The logic was simple: stocks provide growth, bonds provide stability, and when one zigs, the other zags.

Except when they don't.

In 2022, we watched something painful unfold. Rising inflation and aggressive interest rate hikes sent both stocks and bonds tumbling together. The S&P 500 dropped over 18%, and bonds, supposedly the safe haven, fell nearly 13%. The diversification benefit that investors had counted on simply evaporated.

This wasn't a one-time anomaly. Market conditions have changed. Interest rates were near zero for years, which artificially propped up bond prices. As rates normalize, the traditional stock-bond relationship becomes less reliable.

The 40/30/30 model addresses this by adding a third layer of protection. Alternatives often behave independently of public markets, which means your portfolio has multiple shock absorbers instead of just one.

Breaking Down the 30% Alternatives Allocation

Now, "alternatives" is a broad term. It's not just about throwing money at hedge funds and hoping for the best. The 30% allocation can be strategically distributed across several asset types:

Real Estate Direct property investments or private real estate funds that generate income and appreciation independent of stock market swings.

Private Credit Lending directly to companies outside of traditional bank channels. These investments often offer higher yields than public bonds with different risk profiles.

Infrastructure Think toll roads, airports, data centers, and renewable energy projects. These assets tend to have stable cash flows and often come with inflation protection built in.

Private Equity Ownership stakes in private companies that aren't subject to daily market volatility. These investments typically have longer time horizons but can offer substantial returns.

Digital Assets For the forward-thinking investor, institutional-grade exposure to Bitcoin and crypto is becoming a legitimate piece of the alternatives puzzle.

The key is building a diversified alternatives bucket, not just picking one asset class and calling it done. Multiple alternative strategies working together create the uncorrelated returns that actually protect your portfolio.

The Numbers: What Does the Research Say?

Let's talk performance. Because at the end of the day, theory is nice, but results matter.

KKR's research found that the 40/30/30 allocation outperformed the traditional 60/40 portfolio across all timeframes studied. Not some timeframes, all of them.

J.P. Morgan ran the numbers and calculated that adding just 25% to alternative assets could boost 60/40 returns by 60 basis points. That might not sound like much, but on a portfolio expecting 7% annual returns, that's an 8.5% improvement. Over decades, that compounds into serious money.

Here's where it gets interesting from a risk-adjusted perspective. Looking at data from November 2001 through August 2025, a 40/30/30 portfolio achieved a Sharpe ratio of 0.71 compared to just 0.56 for the 60/40 portfolio.

Translation: the 40/30/30 model delivered better returns per unit of risk. You're not just chasing higher returns, you're getting more efficient returns.

Now, the 40/30/30 model did show slightly lower compound annual growth (6.89% vs. 7.46%) over that same period. But here's the trade-off: significantly lower volatility. For many investors, especially those approaching or in retirement, smoother returns are worth more than slightly higher returns on a roller coaster.

What to Consider Before Making the Switch

The 40/30/30 model isn't without its complexities. Here's what you need to know:

Access Can Be Limited Many of the best alternative investments are only available to accredited and institutional investors. Private equity funds, real estate syndications, and private credit vehicles often have minimum investment thresholds that put them out of reach for retail investors.

Fees Are Generally Higher Alternatives typically come with higher management fees than index funds or bond ETFs. You're paying for expertise, access, and the potential for uncorrelated returns. Make sure the value justifies the cost.

Liquidity Trade-offs Unlike stocks that you can sell with a click, many alternative investments lock up your capital for years. This isn't necessarily bad, it can actually protect you from panic selling, but it requires planning.

Manager Selection Matters The dispersion between top-performing and bottom-performing alternative managers is much wider than in public markets. Picking the right partners is critical. A great private equity fund might outperform the average by 10% annually. A poor one might lose money.

It's Not Set and Forget Managing a multi-asset portfolio with alternatives requires more attention than a simple 60/40 allocation. You need to monitor rebalancing, capital calls, distributions, and overall allocation drift.

Is the 40/30/30 Model Right for You?

If you're an accredited or institutional investor looking for:

Better downside protection during market stress

True diversification that actually works when you need it

Access to return streams that aren't tied to public market swings

A more sophisticated approach to long-term wealth preservation

Then yes, the 40/30/30 model deserves serious consideration.

It's not about abandoning public markets. Equities still belong in portfolios. Bonds still have their place. But relying solely on the stock-bond relationship for diversification feels increasingly like bringing a knife to a gunfight.

The investors who thrive in the next decade won't be the ones clinging to outdated frameworks. They'll be the ones who adapt: who recognize that true diversification requires thinking beyond traditional asset classes.

Taking the Next Step

At Mogul Strategies, we specialize in building portfolios that blend traditional assets with innovative alternatives: including institutional-grade digital asset strategies. Our approach is designed specifically for high-net-worth and institutional investors who want more than what conventional portfolios can offer.

The 40/30/30 model isn't just a theory for us. It's the foundation of how we help clients protect and grow wealth in an uncertain world.

Ready to explore what smarter diversification looks like for your portfolio? Visit us at Mogul Strategies to start the conversation.

Comments