The 40/30/30 Portfolio Framework: A Smarter Approach to Diversified Investing in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 19

- 5 min read

If you've been managing money for any length of time, you know the 60/40 portfolio like the back of your hand. Sixty percent stocks, forty percent bonds. Simple. Elegant. And for decades, it worked beautifully.

But here's the thing: the market has changed. And if your allocation strategy hasn't evolved with it, you might be leaving money on the table, or worse, taking on more risk than you realize.

Enter the 40/30/30 portfolio framework. It's not a radical departure from traditional investing. Think of it as an upgrade. One that's designed specifically for the complexities of 2026 and beyond.

What Exactly Is the 40/30/30 Portfolio?

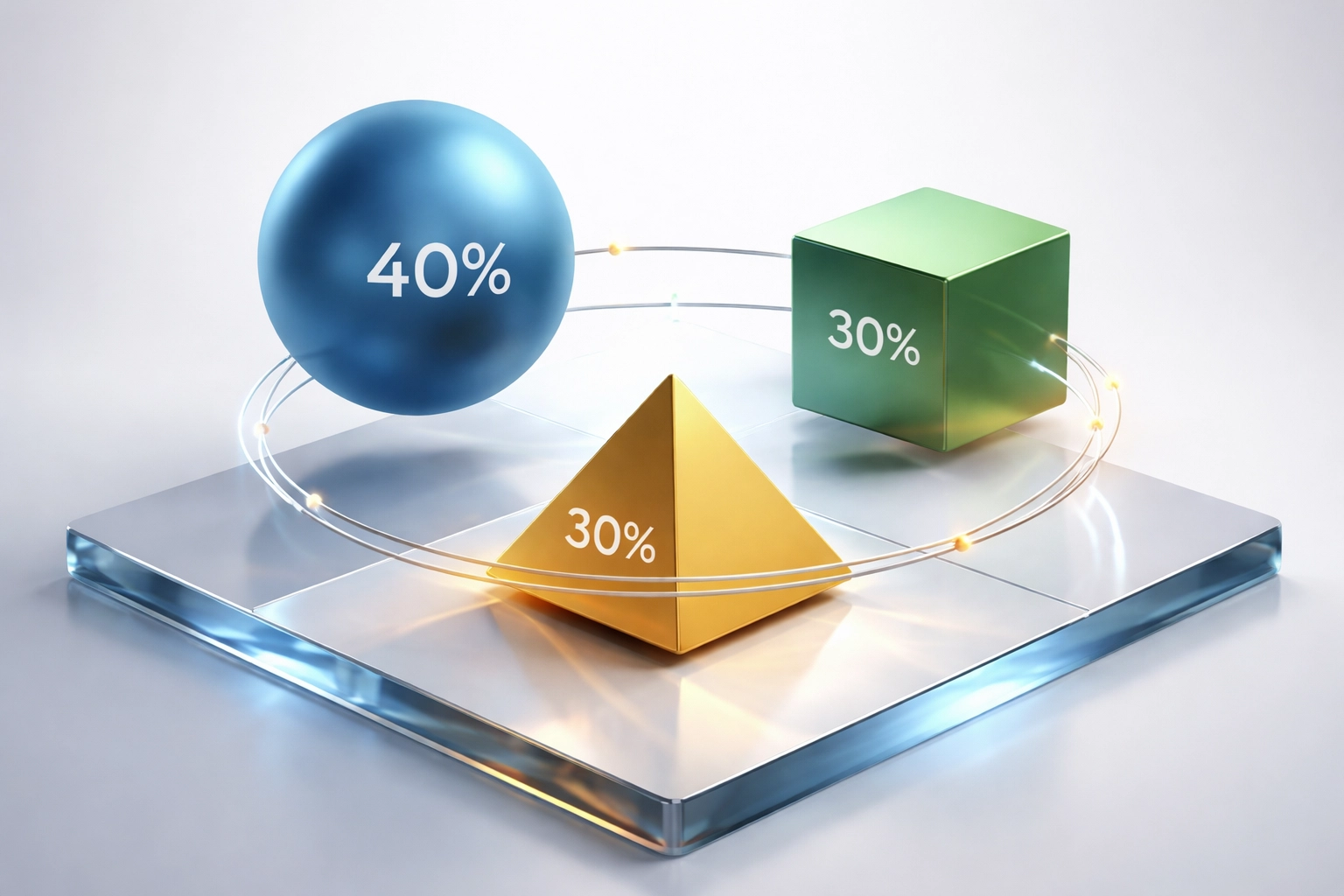

The 40/30/30 framework is straightforward:

40% Equities – Your growth engine

30% Fixed Income – Your stability anchor

30% Alternative Investments – Your diversification edge

That last piece is what makes all the difference. By carving out a dedicated allocation to alternatives, you're introducing a third asset class that doesn't dance to the same tune as stocks and bonds.

And in a world where correlation between traditional assets has become uncomfortably high, that independence is worth its weight in gold.

Why the Classic 60/40 Is Showing Its Age

For years, the 60/40 split was considered the gold standard of portfolio construction. The logic was simple: when stocks dropped, bonds would rise (or at least hold steady), cushioning your portfolio against volatility.

That relationship has fractured.

In 2022, we saw something that rattled even seasoned investors. Both stocks and bonds declined together. Rising inflation and aggressive rate hikes meant there was nowhere to hide. The very diversification benefit that made 60/40 so appealing simply... wasn't there when it mattered most.

And this wasn't a one-off anomaly. Persistent high interest rates, volatile inflation readings, and ongoing geopolitical tensions have fundamentally changed how asset classes interact. Bonds no longer provide the protective buffer they once did.

The 40/30/30 framework acknowledges this new reality. Instead of hoping stocks and bonds will behave like they did in the '90s, it builds in a third pillar specifically designed to preserve capital when the other two move in tandem.

The Numbers Tell a Compelling Story

This isn't just theory. Multiple research institutions have put the 40/30/30 framework under the microscope, and the results are worth paying attention to.

KKR's research found that the 40/30/30 allocation outperformed the traditional 60/40 across all timeframes studied. Not some timeframes. All of them. The framework delivered better returns while simultaneously reducing risk across most macroeconomic environments.

Candriam's analysis went even further, showing a 40% improvement in the Sharpe ratio compared to the 60/40. For those focused on risk-adjusted returns (which should be all of us), that's a significant upgrade in efficiency.

J.P. Morgan's research indicates that even a 25% allocation to alternatives can improve 60/40 returns by approximately 60 basis points. On a portfolio projecting 7% annual returns, that's an 8.5% improvement. Not dramatic, but meaningful, especially compounded over a decade or two.

Looking at longer-term data from November 2001 through August 2025, the picture gets more nuanced. The 40/30/30 portfolio delivered a 6.89% CAGR versus 7.46% for the 60/40. Lower total returns, yes. But here's the catch: the Sharpe ratio came in at 0.71 compared to 0.56 for the traditional allocation.

In plain English? You gave up a bit of return but got significantly more bang for your risk buck. For institutional investors and high-net-worth individuals focused on wealth preservation alongside growth, that trade-off often makes sense.

The Alternative Advantage: What Goes in That 30%?

The "alternatives" bucket is where things get interesting: and where institutional investors have a real edge.

This 30% allocation isn't a monolithic block. It's a toolkit of different strategies, each serving a specific purpose:

Private Credit – Direct lending to companies that banks won't touch. Higher yields, lower correlation to public markets.

Real Estate – Not just REITs, but actual syndicated deals, development projects, and income-producing properties. Tangible assets with inflation hedging characteristics.

Infrastructure – Toll roads, energy facilities, data centers. Long-duration assets with predictable cash flows.

Hedge Fund Strategies – Market-neutral approaches, long/short equity, managed futures. Designed to generate returns regardless of market direction.

Digital Assets – For those with appropriate risk tolerance, a measured allocation to Bitcoin and crypto can provide non-correlated returns and serve as a hedge against monetary policy uncertainty.

The key is that these alternatives provide exposures that don't move in lockstep with your equity or fixed income holdings. When stocks and bonds zig together, well-selected alternatives can zag.

Implementation: The Devil Is in the Details

Let's be honest: implementing a 40/30/30 strategy isn't as simple as buying three ETFs and calling it a day. There are real considerations that separate successful execution from mediocre results.

Fee Awareness

Alternative investments typically come with higher fees than index funds. Private equity might charge 2 and 20. Hedge funds aren't cheap either. You need to ensure that the net returns: after all fees: still justify the allocation. Not all alternatives are created equal, and fee drag can erode the diversification benefits.

Liquidity Management

Many alternatives are illiquid by design. Private credit, real estate syndications, and PE deals can lock up capital for years. This is fine if you've planned for it, but problematic if you need cash in a hurry. Your 30% alternatives allocation needs to account for liquidity matching against your actual needs.

Manager Selection

With public equities, you can buy a low-cost index fund and be done with it. Alternatives require active manager selection. The spread between top-quartile and bottom-quartile managers in private equity, for example, is enormous. Due diligence isn't optional: it's essential.

Dynamic Rebalancing

The framework works best when you're not just "set it and forget it." Different macroeconomic environments call for different tilts within your alternatives bucket. A rising rate environment might favor floating-rate private credit. An inflationary period might call for more real assets. This requires ongoing attention and expertise.

Who Should Consider the 40/30/30 Framework?

This approach isn't for everyone. If you're a retail investor with a $50,000 portfolio and a long time horizon, the classic 60/40 (or even more aggressive allocations) might still make sense.

But if you're an accredited investor, family office, or institutional allocator focused on:

Wealth preservation alongside growth

Reducing portfolio volatility

Accessing non-correlated return streams

Preparing for continued macro uncertainty

...then the 40/30/30 framework deserves serious consideration.

The Bottom Line

The 40/30/30 portfolio isn't about chasing returns or making dramatic bets. It's about acknowledging that the investment landscape has shifted and positioning your portfolio accordingly.

Stocks and bonds will always have their place. But in 2026, relying solely on their historical relationship to protect your wealth is a gamble you don't need to take.

By thoughtfully integrating alternative investments, you can build a portfolio that's more resilient, more efficient, and better equipped to navigate whatever the markets throw at you next.

At Mogul Strategies, we specialize in helping sophisticated investors implement these kinds of frameworks: blending traditional assets with institutional-grade alternatives to build portfolios designed for the long run.

The 60/40 had its moment. Maybe it's time for an upgrade.

Comments