The 40/30/30 Portfolio Framework: How Accredited Investors Are Blending Bitcoin With Traditional Assets in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Feb 2

- 5 min read

The investment landscape has changed. If you're still running a pure 60/40 portfolio in 2026, you're leaving opportunities on the table: and probably taking on more risk than you realize.

Here's what we're seeing with accredited investors this year: a shift toward what we call the 40/30/30 framework. It's not radical. It's not reckless. It's a structured approach to blending traditional assets with Bitcoin and alternatives that actually makes sense for long-term wealth preservation.

Let's break down how this works and why more institutional allocators are making the move.

Why Traditional Allocations Are Breaking Down

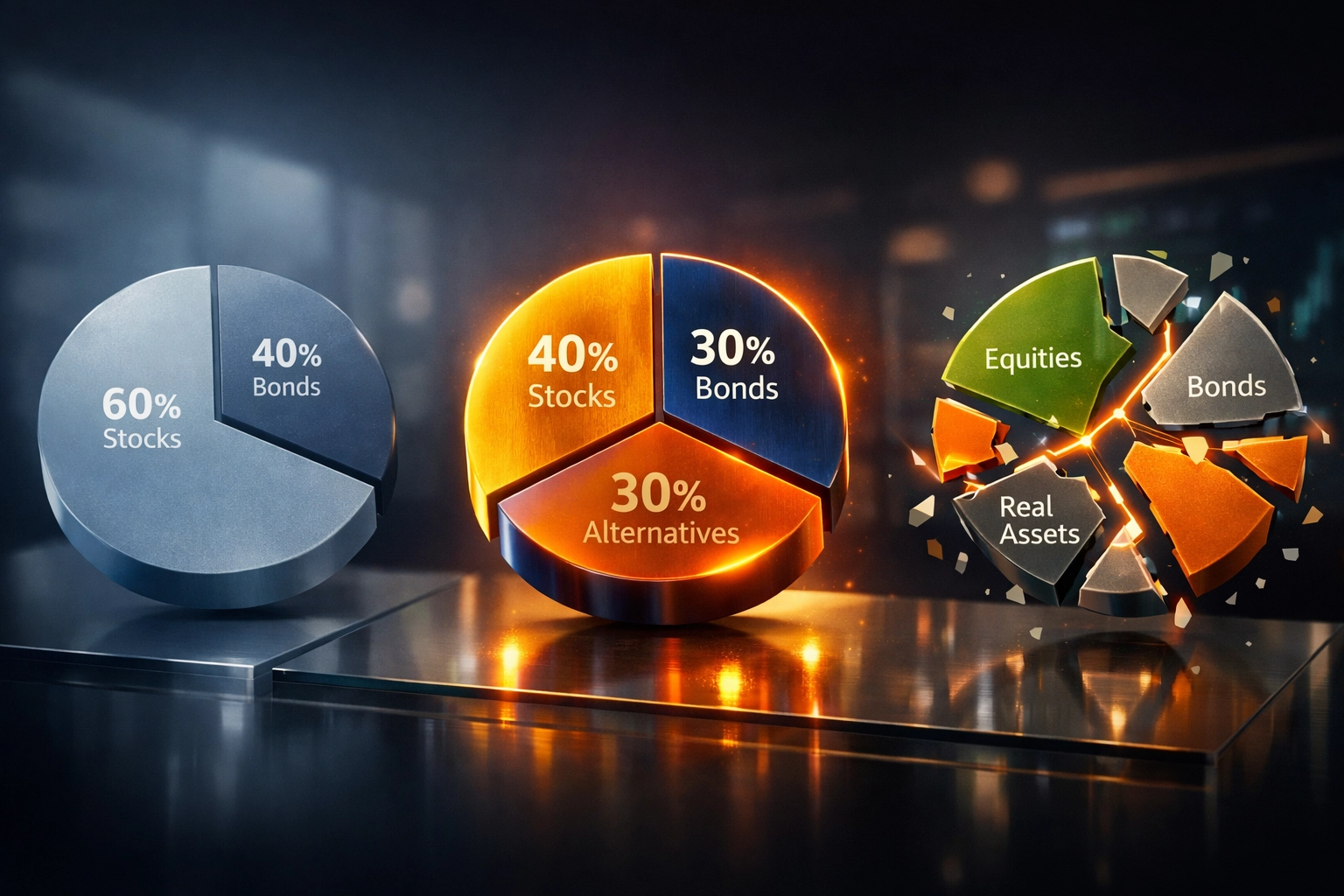

The classic 60/40 portfolio (60% stocks, 40% bonds) worked great for decades. But the correlation between stocks and bonds has been changing. When both asset classes move in the same direction during market stress: like we saw in 2022: that diversification benefit disappears.

Add in persistent inflation concerns, geopolitical uncertainty, and an evolving digital economy, and you've got a recipe for portfolio rethinking.

Smart allocators aren't abandoning traditional assets. They're just being more intentional about what else belongs in the mix.

The 40/30/30 Framework Explained

Here's the basic structure we're implementing for accredited clients:

40% Traditional Core Holdings This is your foundation. Think liquid equities, investment-grade bonds, and treasury exposure. It's not sexy, but it's stable. This portion provides liquidity, generates income, and keeps your portfolio anchored when other positions get volatile.

30% Alternative Assets This bucket includes private equity, real estate syndications, private credit, and managed futures. These are the positions that provide true diversification because they don't move in lockstep with public markets. They also offer access to returns that aren't available in traditional indexes.

30% Digital Assets (Bitcoin-Led) Here's where it gets interesting. This isn't about chasing meme coins or flavor-of-the-month tokens. We're talking about a disciplined allocation to Bitcoin (the majority of this bucket) with selective exposure to institutional-grade digital assets like Ethereum and tokenized real-world assets.

The key word is disciplined. This isn't speculation. It's strategic exposure to an emerging asset class that's increasingly institutional.

Why Bitcoin Deserves a Seat at the Table

Let's address the elephant in the room: Bitcoin still makes some traditional investors uncomfortable. That's fair. But the landscape has shifted dramatically.

In 2026, we're not talking about Bitcoin as some fringe technology. We're talking about:

Spot Bitcoin ETFs with billions in AUM

Public companies holding Bitcoin on their balance sheets

Sovereign wealth funds allocating to digital assets

Banks offering custody solutions for institutional clients

Bitcoin's correlation to traditional assets remains relatively low over longer time horizons, which is exactly what you want in a diversification tool. And its performance characteristics: high volatility but asymmetric upside: make it compelling in a limited allocation.

That last part is critical. We're not suggesting 30% Bitcoin. We're suggesting 30% digital assets with Bitcoin as the anchor (typically 60-75% of that bucket). That means your actual Bitcoin exposure is roughly 18-22% of your total portfolio.

How to Build This Framework (Without Losing Sleep)

Theory is nice. Implementation is what matters. Here's how we approach building a 40/30/30 portfolio:

Start With Dollar-Cost Averaging Into Bitcoin

Don't try to time the market. Build your Bitcoin position over 6-12 months using systematic purchases. This smooths out volatility and removes the emotional element from buying decisions.

For a $5 million portfolio, that means deploying roughly $75,000-$100,000 per month into Bitcoin over the course of a year. Boring? Yes. Effective? Absolutely.

Use Institutional-Grade Custody

If you're holding meaningful Bitcoin exposure, proper custody isn't optional. We're talking qualified custodians with insurance, multi-signature security, and regulatory compliance. This isn't the Wild West anymore.

Rebalance Quarterly, Not Daily

Bitcoin's volatility means it can quickly become oversized (or undersized) in your portfolio. Set calendar reminders to rebalance quarterly. If Bitcoin surges and represents 35% of your portfolio instead of 30%, trim it back and redeploy into other buckets.

This forces you to sell high and buy low automatically.

Layer in Alternatives Thoughtfully

The 30% alternative bucket shouldn't be random. Look for:

Private real estate with 5-7 year hold periods

Private credit opportunities with attractive risk-adjusted yields

PE funds with strong track records and alignment of interests

These positions are illiquid by design. That's a feature, not a bug. They keep you from panic-selling during market drawdowns.

What 2026 Looks Like for This Strategy

We're calling 2026 a consolidation year for digital assets. That means we're likely to see:

Less dramatic volatility than previous cycles

More institutional participation and liquidity

Continued regulatory clarity (which is bullish long-term)

Bitcoin trading in a broader range without extreme moves

This is actually the ideal environment to build or refine a 40/30/30 portfolio. You're not chasing parabolic gains. You're systematically building exposure while volatility is manageable.

For the traditional and alternative portions of the portfolio, we're seeing opportunities in:

Private credit as rates remain elevated

Real estate in select secondary markets with strong demographics

Infrastructure plays benefiting from policy tailwinds

Risk Management Considerations

Let's be clear: this framework isn't risk-free. No portfolio is. But here's how we think about managing risk:

Liquidity Layering: Your 40% traditional core stays liquid. You can access capital quickly if needed. The alternative and digital buckets are longer-term holds.

Correlation Benefits: The three buckets should move independently of each other during most market conditions. That's the whole point.

Downside Protection: Bitcoin can drop 30-40% in a correction. But it's only 20% of your portfolio, meaning a 40% Bitcoin drawdown translates to an 8% portfolio impact. Manageable.

Position Sizing: Never let any single position (including Bitcoin) exceed predetermined thresholds. Discipline beats conviction.

Who This Framework Is For (And Who It Isn't)

The 40/30/30 approach works best for:

Accredited investors with $2M+ in liquid investable assets

Institutional allocators exploring digital asset exposure

Family offices seeking uncorrelated return streams

Investors with 5-10 year time horizons

It's not appropriate for:

Conservative investors who can't stomach volatility

Those needing full liquidity in the next 1-2 years

Anyone treating Bitcoin like a lottery ticket

The Bottom Line

Portfolio construction in 2026 requires thinking beyond traditional boundaries. The 40/30/30 framework isn't about abandoning what works: it's about thoughtfully integrating new asset classes that offer genuine diversification.

Bitcoin isn't the future of your entire portfolio. But it's likely part of the future of diversified portfolios.

If you're an accredited investor or institutional allocator exploring how to integrate digital assets without excessive risk, this framework offers a starting point. It's structured, it's disciplined, and it's designed for the realities of today's market environment.

The question isn't whether portfolios will evolve to include digital assets. The question is whether you'll be early to adapt or late to react.

Comments