The 40/30/30 Portfolio Framework: How Accredited Investors Blend Traditional Assets With Digital Strategies in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Feb 1

- 5 min read

Let's be real: the classic 60/40 portfolio isn't cutting it anymore. If you're still riding that train in 2026, you're probably feeling the pain.

The problem? Stocks and bonds now move together like they're choreographed. When markets tank, both asset classes drop simultaneously. That protective cushion bonds used to provide? Gone. During the 2008 crisis and the 2020 pandemic, traditional 60/40 portfolios lost over 30% of their value: hardly the "conservative" strategy it was sold as.

Accredited investors and institutions have figured this out. They're shifting to what we call the 40/30/30 framework: and they're adding a modern twist that includes digital assets like Bitcoin alongside traditional alternatives.

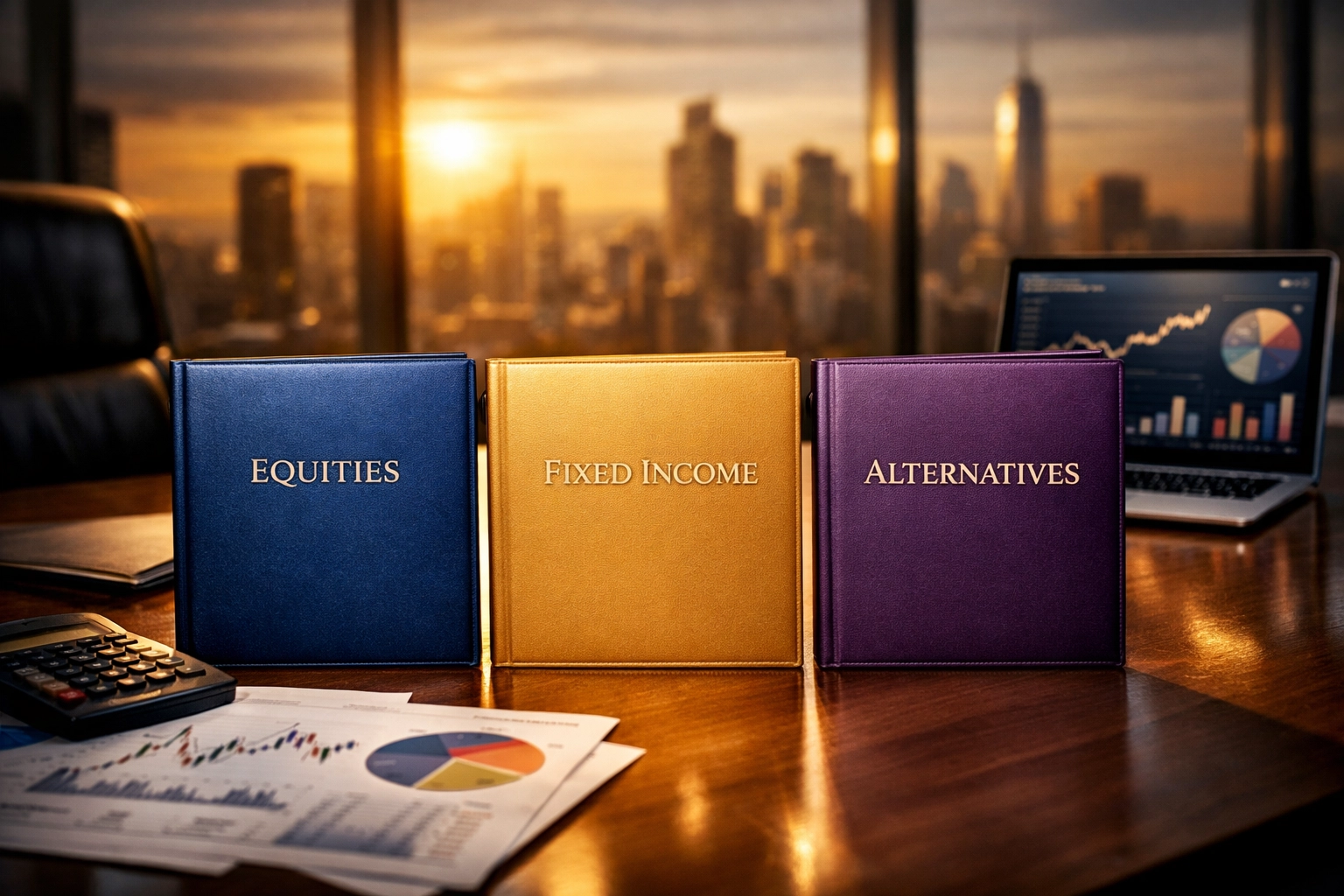

Breaking Down the 40/30/30 Framework

The math is straightforward:

40% Public Equities – Your growth engine

30% Fixed Income – Stability and income generation

30% Alternative Investments – Where things get interesting

This isn't just reshuffling deck chairs. Research shows this approach delivers a 40% improvement in risk-adjusted returns compared to the old 60/40 model. J.P. Morgan's analysis found it generates an extra 60 basis points in returns: that's an 8.5% improvement over the traditional approach's projected 7% return.

The 40% Equities Allocation: Smaller But Smarter

You're probably wondering: "Why only 40% in stocks when the market has been so strong?"

Here's the thing: it's not about timing the market or being pessimistic. It's about not putting all your eggs in one basket, especially when equity valuations are stretched and interest rates remain volatile.

This 40% should still be diversified across sectors, geographies, and market caps. Think global blue chips, emerging markets, and select growth sectors. But by capping it at 40%, you're creating room for assets that actually behave differently when stocks stumble.

The 30% Fixed Income: Not Your Grandfather's Bonds

Fixed income in 2026 looks nothing like it did a decade ago. With interest rate environments constantly shifting, this 30% allocation needs to be dynamic.

Smart money is splitting this bucket between:

Investment-grade corporate bonds for stability

Floating-rate securities that adjust with interest rate changes

Inflation-protected securities (TIPS) to guard against purchasing power erosion

Short-duration strategies to maintain flexibility

The goal isn't massive returns: it's predictable income and downside protection when equity markets get choppy.

The 30% Alternatives: Where Digital Meets Traditional

Here's where the 40/30/30 framework really separates itself from outdated strategies. That 30% alternatives allocation is your diversification powerhouse: and in 2026, it absolutely should include digital assets.

Traditional alternatives still matter:

Private equity for long-term appreciation

Real estate syndications for inflation-hedged cash flow

Private credit for yield in low-rate environments

Hedge fund strategies for uncorrelated returns

Infrastructure investments with built-in inflation adjustments

But forward-thinking accredited investors are carving out 5-10% of this alternatives bucket for institutional-grade Bitcoin and digital asset strategies.

Why Bitcoin Belongs in the Alternatives Allocation

Bitcoin has matured. It's no longer the Wild West speculation it was in 2017. By 2026, we've seen:

Spot Bitcoin ETFs trading for over two years

Major pension funds and endowments holding BTC

Regulatory frameworks providing clarity

Institutional custody solutions offering bank-grade security

More importantly, Bitcoin's correlation to traditional assets remains low over multi-year periods. When you're building a portfolio designed to weather different economic scenarios, you want assets that don't all move in lockstep.

Think of Bitcoin as digital gold: a non-sovereign store of value with a fixed supply cap. In an environment where central banks continue expanding money supply and inflation remains a persistent concern, that matters.

The Functional Role Framework

Candriam Research suggests classifying alternatives by their functional role rather than treating them as one homogeneous block. This is smart thinking.

Your 30% alternatives should be split across three functions:

1. Downside Protection (8-10%) Real estate, infrastructure, and certain hedge fund strategies that provide defensive characteristics and steady cash flows.

2. Uncorrelated Returns (10-12%) Private credit, market-neutral strategies, and yes: Bitcoin and digital assets that move independently of stock/bond correlations.

3. Upside Capture (8-10%) Private equity, venture capital, and growth-oriented alternative strategies that can generate outsized returns during favorable conditions.

This functional approach ensures you're not accidentally loading up on alternatives that all do the same thing.

Performance in Different Market Environments

The 40/30/30 framework shines across various scenarios:

Rising Rate Environment Fixed income moves to shorter durations and floating rates. Alternatives like private credit and real estate with escalation clauses maintain value. Equities have room to breathe at 40% rather than being over-weighted.

Recession The diversified alternatives bucket provides stability. Bitcoin, interestingly, has shown resilience during liquidity events as institutional adoption grows. Fixed income provides the defensive ballast.

High Inflation Real assets in the alternatives bucket: real estate, infrastructure, commodities exposure: along with inflation-protected bonds provide natural hedges. Bitcoin's fixed supply becomes increasingly attractive.

Market Euphoria The 40% equity allocation participates in upside, but you're not overexposed. The discipline of rebalancing back to 40% forces you to take profits when markets run hot.

Implementation for Accredited Investors

Here's the practical reality: building a true 40/30/30 portfolio requires accredited investor status for most people. Many of the highest-quality alternative investments: private equity, real estate syndications, hedge funds: are only available to accredited investors.

Digital asset allocations also work better with scale. You want exposure through institutional-grade custody solutions, not consumer apps. That typically means minimum investments starting at six figures.

The implementation steps:

Audit your current allocation – Most people are shocked to find they're basically running 80/20 or worse

Identify gaps – Where are you over-concentrated?

Phase in alternatives – Don't rush; many alternatives have lock-up periods

Include digital exposure – Start with 3-5% of total portfolio in institutional Bitcoin strategies

Rebalance systematically – Quarterly or semi-annually, back to targets

The 2026 Advantage

What makes this framework particularly relevant in 2026 is the convergence of mature digital asset infrastructure with tested alternative investment strategies.

We're past the experimental phase. Institutional investors have years of data on how Bitcoin behaves in portfolios. Private markets have proven their worth through multiple cycles. Real estate syndications have weathered the 2022-2023 turbulence.

You're not betting on unproven concepts. You're allocating across battle-tested asset classes that happen to be at different maturity stages.

Getting Started

If you're sitting on a traditional portfolio that's basically all stocks and bonds, don't try to flip everything overnight. The beauty of the 40/30/30 framework is that it's systematic.

Start by identifying which alternative investments align with your risk tolerance and time horizon. For most accredited investors, that means exploring a mix of private real estate, select private equity opportunities, and a modest digital asset allocation.

The key is thinking in terms of functional roles: what job is each piece of your portfolio doing? If everything in your portfolio is trying to do the same job (grow when stocks grow), you don't have diversification. You have concentration with extra steps.

The 40/30/30 framework forces you to think differently. And in 2026's complex market environment, different thinking is exactly what your portfolio needs.

Want to explore how the 40/30/30 framework could work for your specific situation?Mogul Strategies specializes in helping accredited investors build portfolios that blend traditional assets with institutional-grade digital strategies. Let's talk about what makes sense for your wealth management goals.

Comments