The Accredited Investor's Guide to Risk Mitigation in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 17

- 5 min read

Let's be honest: being an accredited investor comes with its share of sleepless nights. You've got access to opportunities most people only read about, but that access comes with complexity, uncertainty, and the ever-present question: Am I protecting my downside?

2026 is shaping up to be an interesting year. Markets are stabilizing in some sectors, shifting in others, and the old playbook isn't cutting it anymore. Whether you're sitting on a substantial portfolio or looking to deploy fresh capital, risk mitigation isn't just a nice-to-have. It's the difference between building generational wealth and watching years of work evaporate.

This guide breaks down what actually works right now. No fluff, no jargon-heavy nonsense: just practical strategies you can apply today.

The 2026 Landscape: What's Changed

Before diving into tactics, let's acknowledge where we are. The post-pandemic economic whiplash has mostly settled. Financing conditions are becoming more predictable, particularly in real estate. Lenders are back at the table with clearer terms, especially for stabilized assets.

But here's the thing: stability doesn't mean safety. If anything, it creates a false sense of security that leads to sloppy decision-making. The smart money isn't relaxing right now: it's getting more disciplined.

Interest rates, while potentially easing, remain elevated compared to the easy-money days. Inflation is sticky in some categories. Geopolitical tensions continue creating supply chain hiccups. And digital assets? They're no longer fringe: they're part of serious institutional portfolios.

All of this means risk mitigation in 2026 requires a more nuanced approach than simply "diversify and hope for the best."

The Foundation: Four Pillars of Risk Mitigation

1. Prioritize Proven Operators

This sounds obvious, but you'd be surprised how often sophisticated investors get seduced by slick presentations and bold projections. Here's the reality: track records matter more than optimistic forecasts.

Look for investment teams that have navigated multiple market cycles. Did they survive 2008? How did they handle the 2020 chaos? What about the 2022 rate shock? An operator who's been through the fire and emerged intact has battle-tested systems, relationships, and decision-making frameworks that newcomers simply don't have.

When evaluating sponsors and fund managers, dig into their actual performance during stress periods: not just their up-market returns. Anyone can look good when everything's rising. The real test is how they protect capital when things get ugly.

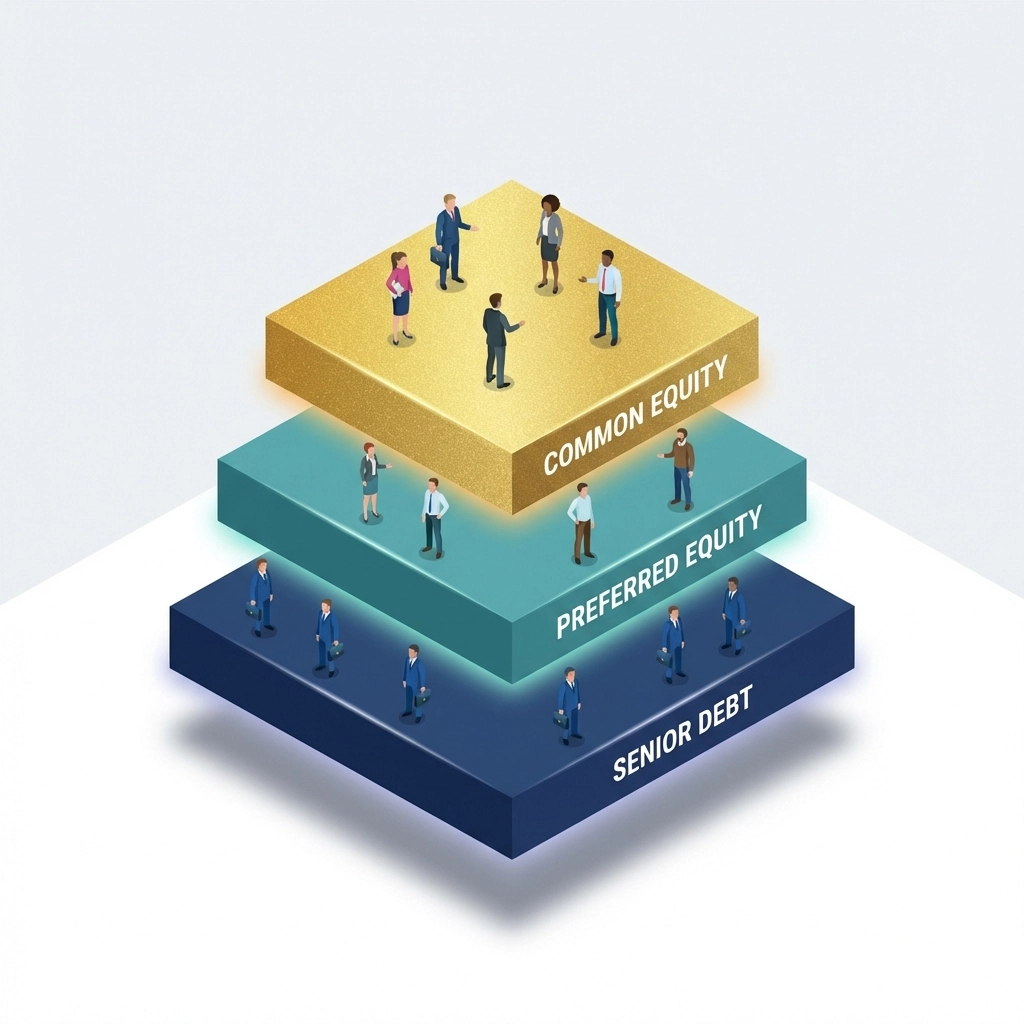

2. Understand Your Position in the Capital Stack

This is where many accredited investors leave money on the table: or worse, take on risks they don't fully understand.

Different positions in an investment's capital structure carry dramatically different risk and return profiles:

Senior debt: First in line for repayment, lowest returns, highest protection

Preferred equity: Middle ground with fixed returns and priority over common equity

Common equity: Highest upside potential, but you're last in line if things go sideways

Knowing exactly where your capital sits determines everything: your downside protection, your recovery priority if the deal struggles, and your realistic return expectations. Don't let anyone gloss over this conversation.

3. Stress-Test Everything

Good underwriting doesn't assume the sun will always shine. It models what happens when clouds roll in.

Before committing capital to any deal, make sure the projections have been stress-tested against tougher conditions:

Lower rents than projected

Higher operating expenses than anticipated

Wider exit cap rates than the base case

Extended stabilization timelines for value-add plays

If a deal only works in the best-case scenario, it's not a good deal: it's a gamble. Solid investments should still generate acceptable returns even when assumptions get haircuts.

This approach is especially critical in sectors like multifamily, where the market is stabilizing but rent growth projections need conservative reality checks.

4. Align Liquidity with Your Actual Needs

This one trips up even experienced investors. Private investments often come with liquidity constraints that look manageable on paper but become painful in practice.

Private credit funds typically limit withdrawals to protect loan performance. Real estate syndications can lock up capital for 3-7 years. Even some hedge fund strategies have gates and redemption windows that restrict access.

Before investing, honestly assess:

Your cash flow needs over the investment horizon

Your ability to weather unexpected expenses without touching these funds

Your emotional tolerance for illiquidity during market stress

Matching your investments' liquidity profiles to your actual life circumstances isn't pessimistic: it's prudent.

Building a Diversified Risk Mitigation Framework

Individual tactics are useful, but the real power comes from combining them into a cohesive framework. Here's an approach that's working well for sophisticated portfolios in 2026:

The Three-Bucket Approach

Bucket 1: Income-Oriented Vehicles

Private credit funds, debt-focused strategies, and other yield-generating investments form your portfolio's foundation. These provide steady, risk-adjusted returns with lower volatility than equity positions. Think of this as your "sleep well at night" allocation.

Bucket 2: Long-Term Equity Positions

Real estate syndications, private equity, and growth-focused investments offer appreciation potential over extended time horizons. These carry more risk but also more upside. The key is patience and quality operator selection.

Bucket 3: Liquid Holdings

Public REITs, liquid alternatives, and traditional market exposure give you flexibility and reduced concentration risk. When opportunities arise or life happens, this bucket provides the maneuverability illiquid positions can't.

The beauty of this framework is balance. Income vehicles generate cash flow. Equity positions build wealth over time. Liquid holdings provide optionality. Together, they create a resilient portfolio that can weather various market conditions.

The Digital Asset Question

We can't have a serious conversation about 2026 portfolio strategy without addressing Bitcoin and crypto. Love it or hate it, institutional-grade digital asset integration is no longer optional for forward-thinking investors.

The key word is "institutional-grade." That means:

Proper custody solutions

Regulated investment vehicles

Clear compliance frameworks

Position sizing appropriate to your risk tolerance

For most accredited investors, this isn't about going all-in on speculation. It's about thoughtful allocation: typically 1-5% of portfolio value: to an asset class with genuinely uncorrelated characteristics and significant long-term potential.

Done right, digital assets can actually enhance your risk mitigation framework rather than undermine it. Done wrong, they become a portfolio liability. The difference is discipline and proper infrastructure.

Sector Spotlight: Multifamily in 2026

Since multifamily often forms a core allocation for accredited investors, it's worth noting the current environment. The sector is entering a more stable phase with increasingly predictable financing. Borrowing costs may ease further, and lenders are returning with clearer terms.

This creates more reliable entry points for passive investors: but doesn't eliminate the need for diligent underwriting. If anything, stability means more competition, which can lead to overpaying if you're not careful.

Focus on:

Operators with proven multifamily track records

Markets with strong employment fundamentals

Deals underwritten with conservative rent growth assumptions

Capital structures that protect downside

Putting It All Together

Risk mitigation isn't a single action: it's a mindset and a process. In 2026, the accredited investors who'll thrive are those who:

Partner with battle-tested operators

Understand exactly where their capital sits in every deal

Demand stress-tested underwriting before committing

Match liquidity to real-world needs

Build diversified frameworks across strategies and time horizons

Stay disciplined even when markets feel stable

The opportunities available to accredited investors in 2026 are genuinely compelling. But opportunity without protection is just speculation with extra steps.

Take the time to build your risk mitigation framework properly. Your future self: the one sleeping soundly while markets do what markets do: will thank you.

Looking for guidance on building a risk-mitigated portfolio that blends traditional assets with innovative strategies? Mogul Strategies specializes in institutional-grade investment approaches for accredited investors.

Comments