The Accredited Investor's Guide to the 40/30/30 Diversification Model in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 18

- 5 min read

If you've been in the investment game for a while, you've probably heard the 60/40 portfolio mentioned more times than you can count. Sixty percent stocks, forty percent bonds: the golden rule of diversification that's been preached since your grandparents started investing.

But here's the thing: the investment landscape in 2026 looks nothing like it did when that model became the standard. And if you're an accredited investor still clinging to 60/40, you might be leaving serious returns on the table while taking on more risk than you realize.

Enter the 40/30/30 model. It's not a radical departure from sound investment principles: it's an evolution. And it might be exactly what your portfolio needs right now.

Why the 60/40 Model Has Lost Its Edge

Let's be honest about what's happening in the markets. The traditional 60/40 portfolio worked beautifully for decades because it relied on one key assumption: when stocks go down, bonds go up (or at least hold steady). This negative correlation was the secret sauce that made diversification actually work.

That assumption? It's broken.

During the financial crises of 2008 and 2020, the 60/40 model exhibited correlation close to 1 with equity markets. Translation: bonds failed to provide the downside protection investors were counting on. When you needed that safety net most, it wasn't there.

And it gets worse. In today's macroeconomic environment, stocks and bonds have started moving in tandem. The correlation between equities and bonds has turned positive, which fundamentally undermines the diversification benefit that made 60/40 effective in the first place.

Add in volatile inflation, elevated interest rates constraining equity valuations, and bonds offering reduced returns with diminished protective capacity: and you've got a recipe for underwhelming performance.

So what's the alternative?

Breaking Down the 40/30/30 Model

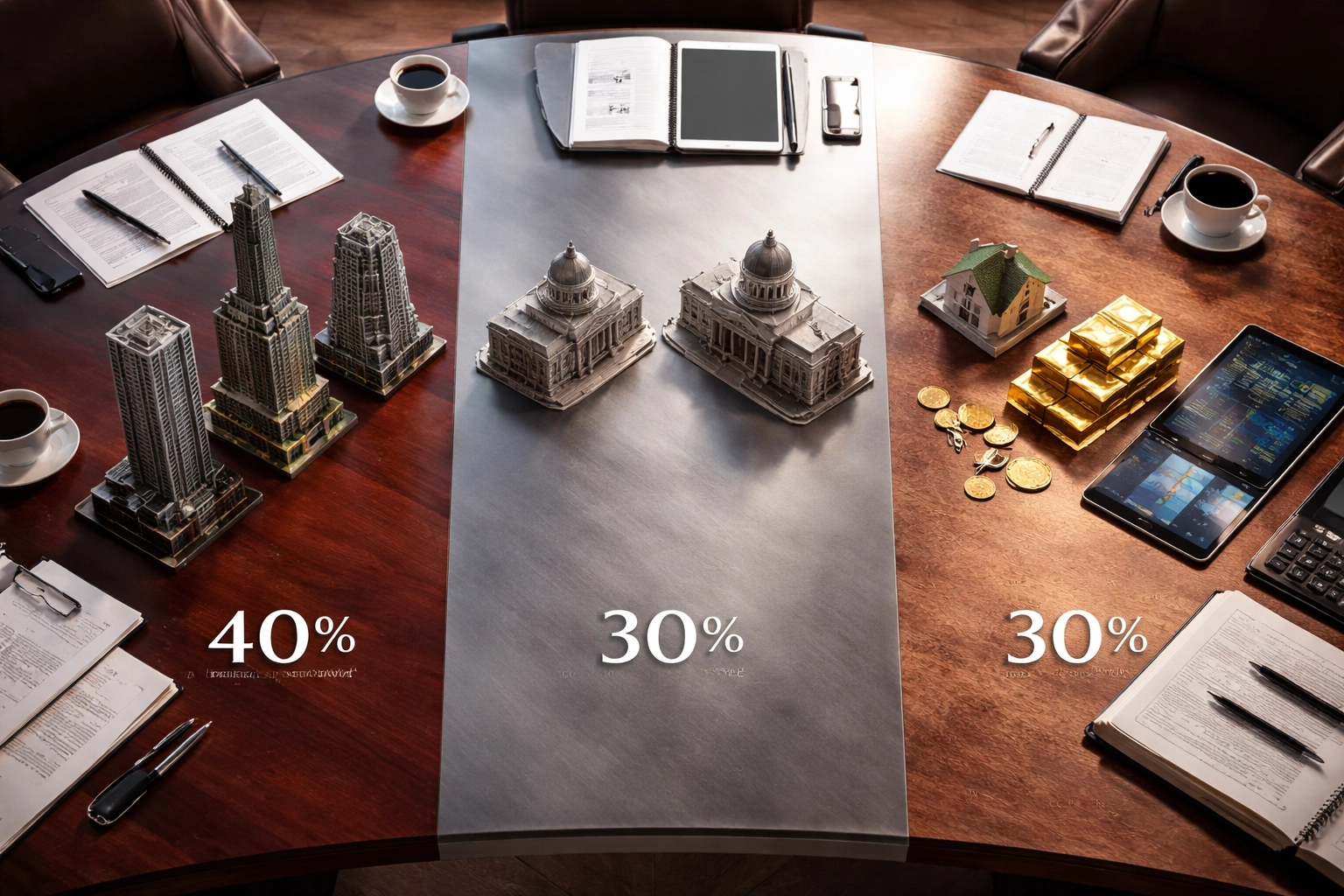

The 40/30/30 portfolio is straightforward:

40% in public equities : Your growth engine

30% in fixed income : Your stability anchor

30% in alternative investments : Your diversification supercharger

That 30% alternatives allocation is where things get interesting for accredited investors. This isn't about chasing the latest trend or speculating on meme stocks. It's about accessing the same institutional-grade strategies that pension funds, endowments, and family offices have been using for decades.

While institutions have leveraged alternatives for years: often allocating over 40% of their assets to them: the 40/30/30 framework makes this institutional resilience accessible to individual accredited investors who qualify.

The Numbers Don't Lie: Performance Advantages

Let's talk results, because that's what matters.

Research shows the 40/30/30 allocation delivers a 40% improvement in its Sharpe ratio compared to the traditional 60/40 model. For those who need a refresher, the Sharpe ratio measures risk-adjusted returns: essentially how much return you're getting for each unit of risk you're taking on.

A 40% improvement isn't marginal. That's significant.

J.P. Morgan's analysis found that adding just a 25% allocation to alternatives can enhance 60/40 returns by 60 basis points. That represents an 8.5% improvement to the 60/40 portfolio's projected 7% return. Over a multi-decade investment horizon, that difference compounds dramatically.

KKR's research confirmed that 40/30/30 outperformed 60/40 across all timeframes studied, while simultaneously delivering lower volatility and more controlled drawdowns. You're getting better returns with less stomach-churning downside. That's the holy grail of portfolio construction.

How to Actually Implement This

Here's where the rubber meets the road. Having a 30% alternatives allocation is one thing: knowing what to put in it is another.

One of the most practical frameworks comes from Candriam's functional allocation approach. Instead of treating alternatives as one homogeneous block, they recommend classifying alternative assets according to three functional roles:

1. Downside Protection These are assets that provide cushion during market declines. Think hedging strategies, certain types of managed futures, or assets with low correlation to equity markets.

2. Generation of Uncorrelated Returns Investments that move independently from stocks and bonds. This is where strategies like market-neutral hedge funds, certain commodities, and select private credit opportunities come into play.

3. Capture of Upside Potential Strategies designed to benefit from market growth, including private equity, venture capital, and growth-oriented real assets.

This functional segmentation isn't just academic theory. It enables dynamic rebalancing according to macroeconomic conditions, which is far more sophisticated than a static "set it and forget it" allocation.

What Should Go in Your Alternatives Sleeve?

For accredited investors in 2026, several alternative asset classes deserve serious consideration:

Infrastructure and Real Estate

These are particularly valuable because they often feature inflation-adjustment clauses built into underlying contracts. As consumer prices rise, your returns adjust accordingly. In an environment where inflation remains unpredictable, this natural hedge is incredibly valuable.

Real estate syndication deals, in particular, offer accredited investors access to institutional-quality properties without the hassle of direct ownership.

Private Credit

This has emerged as a major focus area. KKR recommends a 10% allocation within the alternatives sleeve given recent market opportunities. With traditional banks pulling back from certain lending activities, private credit fills the gap: often with attractive risk-adjusted yields.

Hedge Fund Strategies

Market-neutral and long/short strategies can provide genuine diversification benefits. The key is selecting managers with proven track records and strategies that genuinely offer uncorrelated returns, not just equity beta in disguise.

Digital Assets

For investors with appropriate risk tolerance, institutional-grade Bitcoin and crypto integration has matured significantly. This isn't the Wild West of 2021: we're talking about custody solutions, regulated vehicles, and sophisticated allocation frameworks that make sense for accredited portfolios.

Key Considerations Before You Jump In

The transition to 40/30/30 isn't about abandoning diversification principles. It's about updating them for an environment where traditional asset class correlations have fundamentally changed.

A few things to keep in mind:

Liquidity requirements matter. Many alternative investments have lockup periods. Make sure your overall portfolio maintains enough liquidity for your needs.

Due diligence is non-negotiable. Not all alternatives are created equal. Manager selection, fee structures, and alignment of interests all require careful evaluation.

Active allocation beats passive. Unlike a simple index fund approach, alternatives benefit from active, centralized allocation that responds to real-time market changes.

Start with a realistic timeline. Many alternatives show their value over full market cycles. If you're measuring performance quarter by quarter, you might get discouraged before the strategy has time to work.

The Bottom Line

Financial advisers are increasingly exploring lower fixed income allocations and building momentum toward the 40/30/30 model, though adoption remains in its early phases. As an accredited investor, you have the opportunity to be ahead of this curve rather than catching up later.

The 40/30/30 model isn't about chasing returns or taking unnecessary risks. It's about recognizing that the investment landscape has evolved and your portfolio strategy should evolve with it.

At Mogul Strategies, we specialize in blending traditional assets with innovative strategies: including institutional-grade alternatives: to help high-net-worth investors build more resilient portfolios. The 40/30/30 model is just one tool in the arsenal, but it's one that more accredited investors should seriously consider in 2026 and beyond.

The old rules still apply: diversify, think long-term, and manage risk. How you implement those rules? That's what needs updating.

Comments