The Accredited Investor's Guide to the 40/30/30 Diversification Model in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 19

- 5 min read

If you've been investing for any length of time, you've probably heard of the classic 60/40 portfolio. Sixty percent stocks, forty percent bonds. Simple. Elegant. And for decades, it worked beautifully.

But here's the thing: the market conditions that made 60/40 effective have fundamentally changed. And if you're still relying on that old playbook in 2026, you might be leaving money on the table, or worse, exposing yourself to risks you didn't sign up for.

Enter the 40/30/30 diversification model. It's not just a tweak to the old formula. It's a complete rethinking of how sophisticated investors can build resilient, growth-oriented portfolios in today's environment.

Let's break it down.

Why the 60/40 Portfolio Has Lost Its Edge

The 60/40 portfolio was built on one key assumption: when stocks go down, bonds go up (or at least hold steady). This negative correlation meant your portfolio had a built-in shock absorber.

That assumption? It's basically broken.

Research now shows that the long-term correlation between equities and fixed income has climbed to near 1.0. In plain English: stocks and bonds are moving together more often than not. When the market tanks, your bonds aren't providing the safety net they used to.

Add in persistent inflation pressures and a "higher for longer" interest rate environment, and you've got a recipe for underperformance. The risk-return profile of both asset classes has shifted, and portfolios need to adapt.

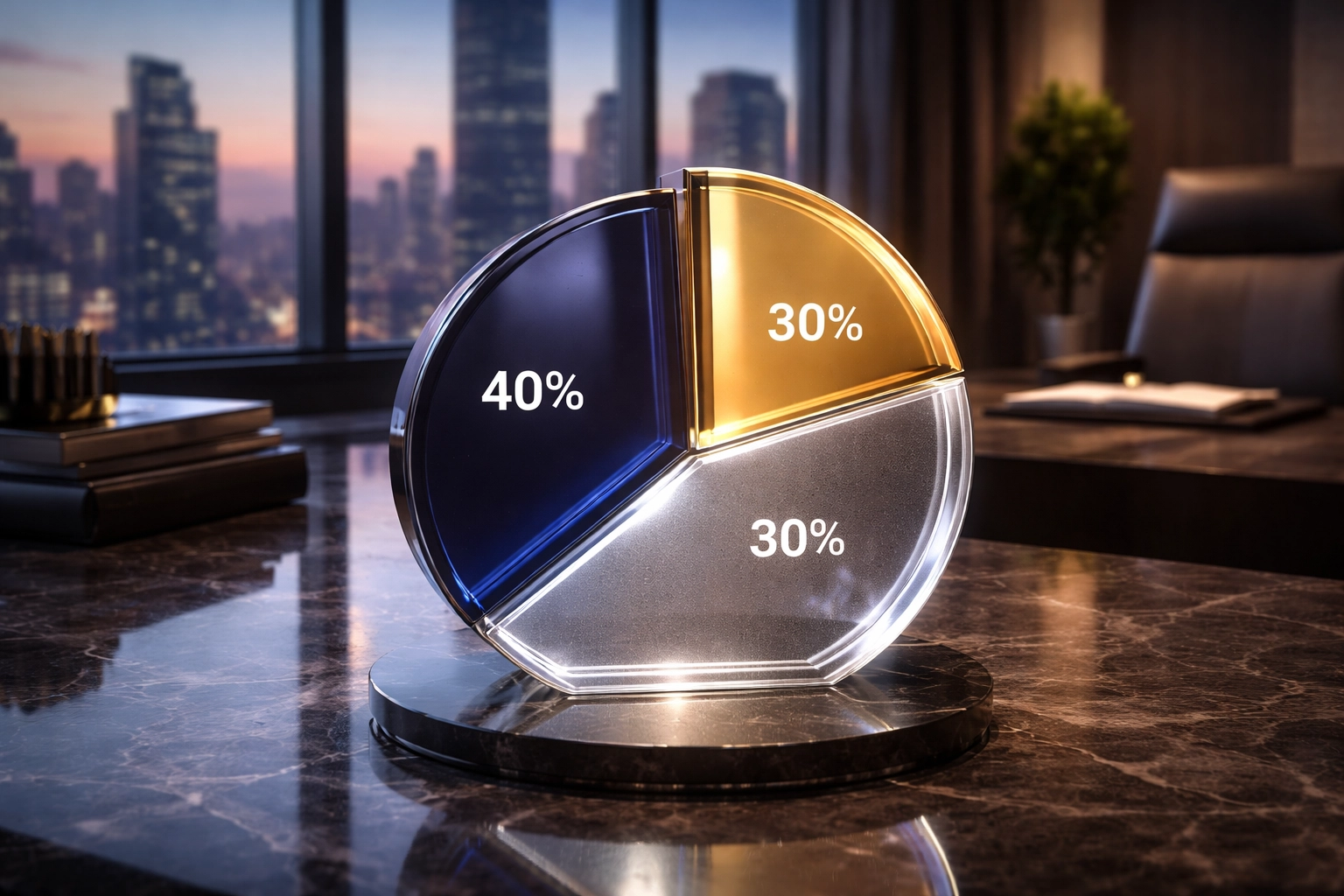

What Is the 40/30/30 Model?

The 40/30/30 portfolio is straightforward:

40% Public Equities

30% Fixed Income

30% Alternative Investments

That 30% allocation to alternatives is the game-changer. By introducing assets that operate with lower correlation to traditional stocks and bonds, you're restoring the diversification benefits that the 60/40 model has lost.

Think of it as upgrading your portfolio's immune system. You're not eliminating risk, you're building in resilience.

Breaking Down the Three Components

Let's look at each piece of the puzzle and why it matters for accredited investors in 2026.

Public Equities (40%)

Yes, you're reducing your stock exposure compared to the traditional model. But 40% still gives you meaningful growth potential. The key difference is acknowledging reality: in an environment where stocks and bonds are increasingly correlated, concentrating 60% of your portfolio in equities creates more risk than it used to.

This 40% allocation should still be thoughtfully diversified across:

Domestic and international markets

Growth and value styles

Large, mid, and small-cap companies

The goal isn't to abandon equities. It's to right-size them for today's market dynamics.

Fixed Income (30%)

Bonds still have a role to play, but it's a supporting role rather than a co-starring one. The reduced 30% allocation reflects the reality that traditional fixed income just isn't delivering the same risk-adjusted returns it once did.

Smart implementation here often means going beyond plain vanilla bonds. Many advisers now recommend enhancing this sleeve with private credit: floating rate assets that boost income generation and shorten duration while providing additional diversification benefits.

Private credit has become increasingly accessible to accredited investors, and it offers yields that traditional investment-grade bonds simply can't match right now.

Alternatives (30%)

This is where the 40/30/30 model really shines for accredited investors.

The alternatives sleeve typically includes:

Private Equity: Access to companies before they go public, with potential for outsized returns

Private Credit: Higher-yielding debt instruments outside traditional bond markets

Real Estate: Direct ownership or syndications with income and appreciation potential

Infrastructure: Essential assets like utilities, transportation, and energy facilities

Here's what makes alternatives particularly valuable right now: many of these assets: especially infrastructure and real estate: have inflation adjustment clauses built into their contracts. When consumer prices rise, your income rises with them. That's a natural hedge you simply don't get from stocks or bonds.

These assets have also historically demonstrated reduced correlation to public markets, which is exactly what your portfolio needs when traditional diversification isn't working.

The Numbers Don't Lie

If you're skeptical about whether this approach actually delivers, let's look at what the research shows.

J.P. Morgan found that adding a 25% allocation to alternatives can boost 60/40 returns by 60 basis points. That might sound small, but it represents an 8.5% improvement to the projected 7% return of a traditional 60/40 portfolio. Over a multi-decade investment horizon, that compounds into serious money.

KKR research went even further, demonstrating that the 40/30/30 model outperformed the 60/40 across all timeframes studied.

Candriam's 25-year analysis showed that even the simplest 40/30/30 allocation enhanced returns while simultaneously reducing both volatility and drawdown compared to the traditional mix.

Better returns. Lower risk. That's not a tradeoff: that's a free lunch (or as close as you get in investing).

Why This Matters Now for Accredited Investors

Here's the exciting part: portfolios like this used to be reserved for massive institutions and ultra-high-net-worth families. If you wanted meaningful alternative allocations, you typically needed $500,000+ minimums and institutional connections.

That landscape has transformed dramatically.

New fund structures, investment platforms, and wealthtech innovations have lowered barriers to entry. As an accredited investor, you can now construct portfolios that previously were available only to pension funds and endowments.

This democratization of access is one of the most significant shifts in wealth management in the past decade. And at Mogul Strategies, we believe it creates an unprecedented opportunity for accredited investors to build truly institutional-quality portfolios.

Implementing the 40/30/30 Model

So how do you actually put this into practice? Here are some key considerations:

Within the Alternatives Sleeve

KKR specifically advocates for allocating 10% to private credit in the current environment, given recent market pullbacks creating attractive entry points. The remaining 20% can be distributed across infrastructure, real estate, or other diversifying alternatives based on your specific situation.

Liquidity Planning

Unlike stocks and bonds, alternatives often have lock-up periods. You need to ensure you have adequate liquid assets for near-term needs before committing capital to longer-duration investments.

Time Horizon

The 40/30/30 model works best for investors with a medium to long-term horizon (5+ years). If you need access to all your capital within the next few years, this approach may need modification.

Professional Guidance

The alternatives space can be complex. Working with experienced advisers who understand both traditional and alternative investments is crucial for effective implementation.

The Industry Is Moving This Direction

It's worth noting that financial advisers across the industry are increasingly adopting 40/30/30 or similar models (such as 60/20/20). This signals a shifting consensus about the inadequacy of traditional 60/40 construction.

You don't have to be an early adopter here. The smart money has already validated this approach. The question is whether you'll update your portfolio to reflect market realities: or stick with a strategy designed for a different era.

Building Your 2026 Portfolio

The 40/30/30 model isn't a magic bullet. No investment strategy is. But it represents a thoughtful evolution of portfolio construction that addresses the real challenges facing investors today:

Rising correlations between stocks and bonds

Persistent inflation pressures

A higher interest rate environment

The need for genuine diversification

For accredited investors, the opportunity to build institutional-quality portfolios has never been more accessible. The question isn't whether the 40/30/30 approach makes sense: the research clearly supports it. The question is how to implement it in a way that fits your unique goals, timeline, and risk tolerance.

At Mogul Strategies, we specialize in helping accredited investors blend traditional assets with innovative alternative strategies. If you're ready to explore what a modernized portfolio could look like for you, we'd love to have that conversation.

Comments