The Accredited Investor's Guide to the 40/30/30 Diversified Portfolio Model in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 19

- 5 min read

If you've been investing for any length of time, you've probably heard about the classic 60/40 portfolio. Sixty percent stocks, forty percent bonds. Simple. Elegant. And increasingly... inadequate.

Here's the thing: the 60/40 worked brilliantly for decades. But we're not living in those decades anymore. Volatile inflation, stubborn interest rates, geopolitical chaos, and bonds that just aren't pulling their weight have fundamentally changed the game.

That's where the 40/30/30 model comes in. It's not revolutionary: institutional investors have been using variations of this for years. But it's becoming essential for accredited investors who want to build portfolios that actually hold up when things get rough.

Let me walk you through what this model looks like, why it matters, and how you can start implementing it in 2026.

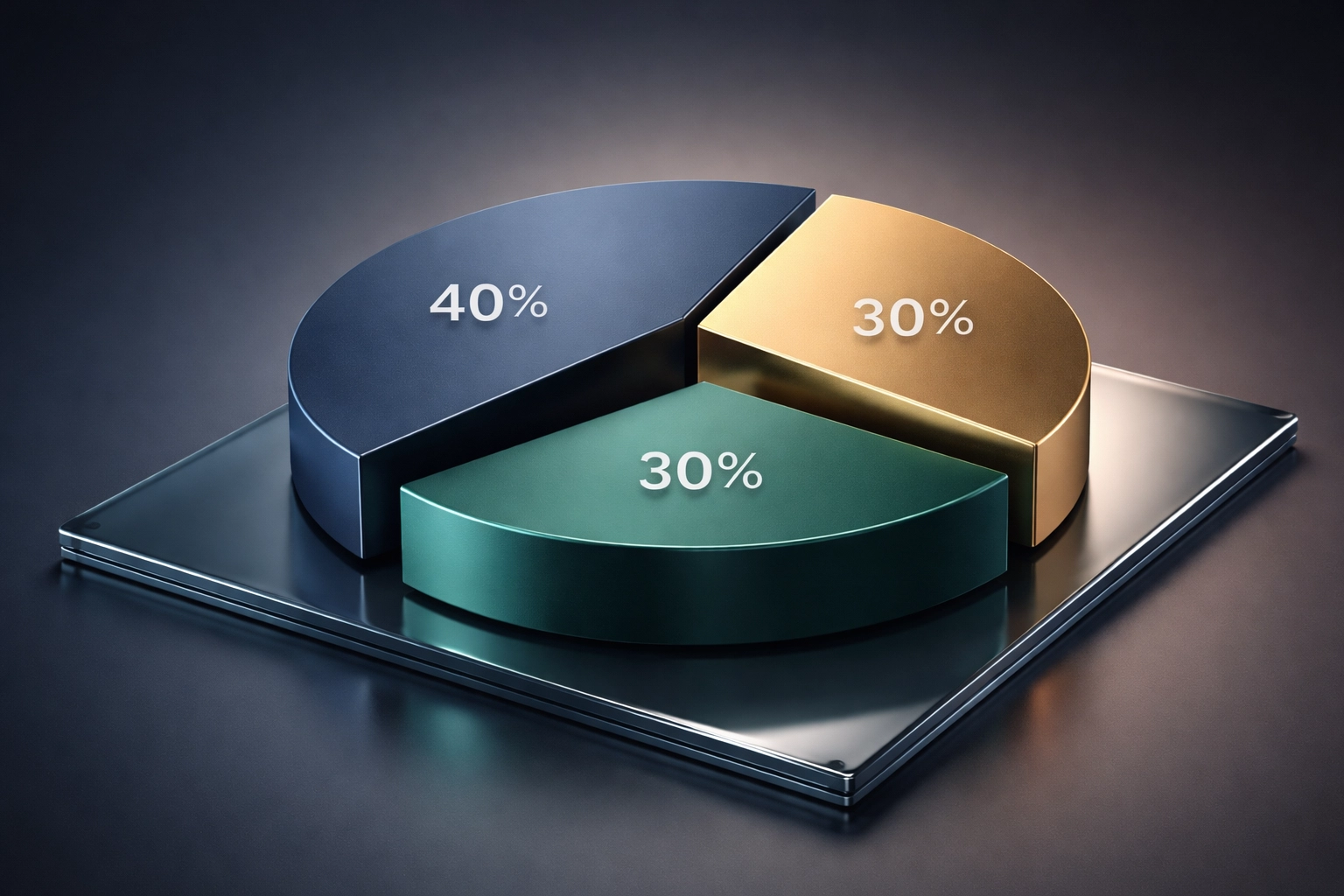

What Exactly Is the 40/30/30 Portfolio?

The 40/30/30 portfolio is a modernized approach to diversification that allocates your assets like this:

40% to public equities (stocks, ETFs, index funds)

30% to fixed income (bonds, treasuries, credit instruments)

30% to alternative investments (private equity, real estate, hedge funds, crypto, and more)

Think of it as the 60/40's evolved cousin. You're still getting exposure to traditional markets, but you're carving out a significant chunk for assets that move to their own beat.

The key difference? That 30% alternatives allocation. It's not just a nice-to-have anymore: it's becoming the backbone of portfolio resilience for sophisticated investors.

Why the 60/40 Portfolio Has Lost Its Edge

Let's be honest about what happened to the 60/40.

During market crises in 2008 and 2020, portfolios built on the 60/40 model experienced losses exceeding 30%. That's not exactly the "balanced" outcome investors were hoping for.

The problem is correlation. When markets tank, the 60/40 portfolio tends to move almost in lockstep with equities. Research shows correlation approaching 1 during crisis periods: meaning your "diversified" portfolio is essentially behaving like an all-stock portfolio at the worst possible times.

Add to that the current environment:

Inflation volatility that makes fixed returns less predictable

Higher interest rates that have hammered bond values

Geopolitical uncertainty that creates sudden market shocks

Reduced protective capacity from bonds in general

The 60/40 was designed for a world with more stable inflation, lower rates, and less global interconnection. That world doesn't exist anymore.

The Performance Case for Going 40/30/30

Here's where it gets interesting. The numbers actually back up this shift.

Research from major institutions like J.P. Morgan and KKR has demonstrated consistent outperformance from portfolios that incorporate meaningful alternative allocations:

40% improvement in Sharpe ratio (that's your risk-adjusted return: the holy grail of portfolio metrics)

Higher absolute returns with lower volatility

Better downside protection during market corrections

J.P. Morgan's analysis found that adding 25% in alternatives improves the projected 7% return of a 60/40 by about 60 basis points: an 8.5% enhancement

KKR's research took it further, showing that the 40/30/30 approach outperformed the traditional 60/40 across every timeframe they studied. Not some timeframes. All of them.

This isn't about chasing returns. It's about building a portfolio that doesn't fall apart when you need it most.

Breaking Down the Alternatives Bucket

Here's where a lot of investors get tripped up. "Alternative investments" sounds like one thing, but it's actually a massive category with wildly different behaviors.

Not all alternatives are created equal. Candriam's research suggests categorizing them by their functional role in your portfolio rather than treating them as a homogeneous group:

Downside Protection

These are strategies designed to hedge against market declines. Think managed futures, certain hedge fund strategies, or protective options overlays. When stocks drop, these should help cushion the blow.

Uncorrelated Returns

Assets that move independently of stocks and bonds. Private credit, litigation finance, certain real estate strategies, and infrastructure investments often fall here. They're not necessarily counter-cyclical: they just march to their own drummer.

Upside Capture

Strategies positioned to benefit from market opportunities. Private equity, growth-oriented real estate, and yes: strategically allocated digital assets like Bitcoin can fall into this category.

The smart play is building your alternatives allocation with all three roles in mind. You want some protection, some true diversification, and some growth potential that isn't tied to public market cycles.

Accessibility Has Changed the Game

Here's the good news: this isn't just for the ultra-wealthy anymore.

A decade ago, getting into private markets meant writing checks of $500,000 or more. The barriers were deliberately high. But the landscape has shifted dramatically.

New fund structures, improved platforms, and wealthtech innovations have opened doors that were previously closed. As an accredited investor, you can now access:

Private equity through feeder funds and interval funds

Private credit with more reasonable minimums

Real estate syndications at various entry points

Infrastructure investments through new vehicle structures

Digital asset strategies with institutional-grade custody and management

This democratization means the portfolio resilience that was once exclusive to endowments and family offices is now within reach for a much broader group of sophisticated investors.

Implementation: Getting This Right

Having the right framework is step one. Executing it well is step two: and it's where many investors stumble.

Active Management Matters

With alternatives, passive doesn't really exist the same way it does with index funds. The dispersion between top-quartile and bottom-quartile managers in private equity, for example, is enormous. Selecting the right strategies and managers can make or break your alternatives allocation.

Think Functionally

When you're adding an alternative investment, ask yourself: what role is this playing? If your entire alternatives bucket is oriented toward upside capture, you've missed the point. Balance across the three functional roles we discussed earlier.

Rebalance Dynamically

The 40/30/30 isn't a set-it-and-forget-it model. Macroeconomic conditions shift, and your allocation should respond. When recession risk rises, you might lean more heavily into downside protection. When growth looks strong, upside capture strategies might deserve more weight.

Understand Liquidity Trade-offs

Many alternative investments come with lock-up periods or limited redemption windows. This is a feature, not a bug: it's part of what generates their premium returns. But you need to understand your liquidity needs and structure accordingly.

Where Digital Assets Fit In

You might be wondering where crypto and Bitcoin fit into this picture. For accredited investors in 2026, institutional-grade digital asset strategies are increasingly being incorporated into the alternatives bucket.

The key is approaching them the same way you'd approach any alternative: with clear functional intent, proper risk management, and professional-grade execution. This isn't about speculation: it's about accessing a genuinely uncorrelated asset class with defined allocation limits.

At Mogul Strategies, we've been focused on blending traditional assets with innovative digital strategies in a way that makes sense for sophisticated portfolios. It's about integration, not replacement.

The Bottom Line

The 40/30/30 model isn't about abandoning traditional investing. It's about evolving it.

Public equities still matter. Fixed income still has a role. But in 2026's environment, limiting yourself to just those two asset classes leaves you exposed in ways that weren't true a generation ago.

For accredited investors willing to embrace a more sophisticated approach, the 40/30/30 framework offers a path to genuine diversification: the kind that actually shows up when you need it.

The institutional investors figured this out years ago. Now it's your turn.

Comments