The Accredited Investor's Guide to the 40/30/30 Portfolio Model in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 25

- 5 min read

If you've been investing for a while, you've probably heard of the 60/40 portfolio. For decades, it was the gold standard: 60% stocks for growth, 40% bonds for stability. Simple. Elegant. And for a long time, it worked.

But here's the thing: 2026 isn't the same market we had ten or twenty years ago. Volatile inflation, unpredictable interest rates, and geopolitical tensions have fundamentally changed the game. The 60/40 model? It's showing its age.

Enter the 40/30/30 portfolio model. It's gaining serious traction among institutional investors and high-net-worth individuals who want something more resilient. Let's break down what it is, why it matters, and how you can put it to work.

Why the 60/40 Portfolio Has Lost Its Edge

The 60/40 portfolio was built on a simple premise: stocks and bonds move in opposite directions. When stocks tank, bonds rise to cushion the blow. Nice theory. But recent history tells a different story.

During the 2008 financial crisis and the 2020 pandemic-driven market collapse, the 60/40 portfolio showed correlation close to 1 with the equity market. Translation? It dropped nearly as hard as stocks alone. The "protection" investors expected simply wasn't there.

And it's not just about crisis moments. Today's environment of sticky inflation, higher-for-longer interest rates, and synchronized movement between stocks and bonds means the traditional model struggles to deliver consistent risk-adjusted returns.

For accredited investors looking to preserve and grow wealth, relying solely on the 60/40 split is like driving with outdated GPS: you might eventually get where you're going, but you'll hit a lot of unnecessary roadblocks.

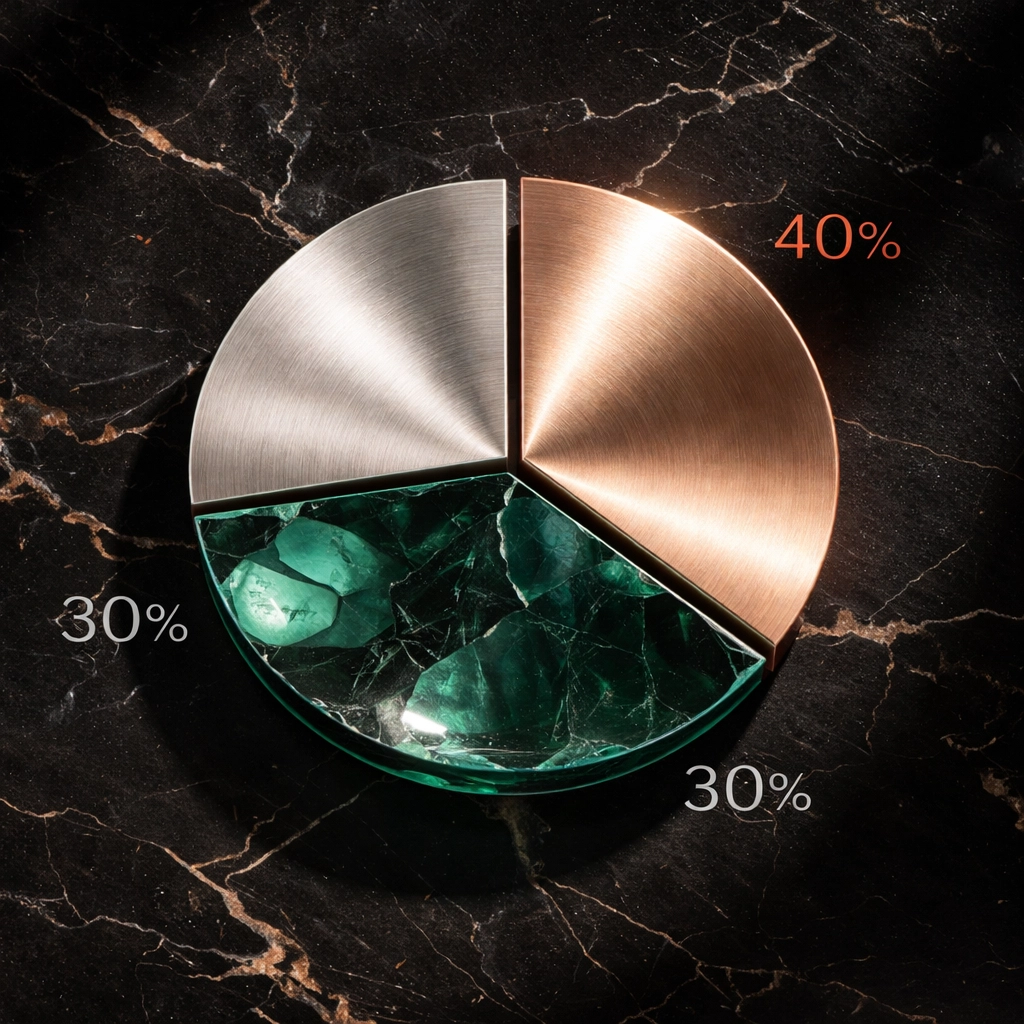

What Is the 40/30/30 Portfolio Model?

The 40/30/30 portfolio takes a more modern approach to allocation:

40% Public Equities – Still your primary growth engine, but reduced from the traditional 60%

30% Fixed Income – Acknowledges bonds' more constrained returns and limited protective capacity today

30% Alternative Investments – The game-changer that provides diversification, reduced correlation, and resilience

This isn't just theoretical. Historical analysis shows the 40/30/30 portfolio achieved a 40% improvement in its Sharpe ratio compared to the 60/40 model. For those unfamiliar, the Sharpe ratio measures risk-adjusted returns, basically, how much return you're getting for each unit of risk you're taking.

Research from J.P. Morgan found that adding just a 25% allocation to alternative assets can improve 60/40 returns by 60 basis points: an 8.5% improvement. KKR's analysis similarly showed 40/30/30 outperformed 60/40 across all timeframes they studied.

The numbers don't lie. This framework works.

The Secret Sauce: Understanding Alternative Investments

Here's where things get interesting. That 30% allocation to alternatives isn't a monolithic category. Not all alternatives behave the same way under different market conditions.

Smart portfolio construction means classifying alternatives by their functional role. Think of it like building a sports team: you need different positions working together, not just the best individual players.

The Three Functions of Alternatives

1. Downside Protection Strategies

These are your defensive players. They're designed to preserve capital during market stress. Think managed futures, certain hedge fund strategies, or assets with low correlation to equity markets. When everything else is dropping, these holdings help keep your portfolio afloat.

2. Uncorrelated Return Generators

These strategies provide returns independent of stocks and bonds. Private credit, litigation finance, and certain real asset strategies fall into this bucket. They march to their own beat, which is exactly what you want when traditional markets move in lockstep.

3. Upside Potential Capture

These are your growth-oriented alternatives: private equity, venture capital, and opportunistic real estate. They're designed to capture market opportunities and generate alpha beyond what public markets offer.

The magic happens when you balance all three functions within your alternative allocation. This gives you a portfolio that can defend, diversify, and attack depending on market conditions.

Alternative Assets: Now More Accessible Than Ever

Here's some good news. Less than a decade ago, getting into private markets typically required $500,000 or more as a minimum investment. That left most accredited investors on the sidelines.

Not anymore.

New fund structures, investment platforms, and wealthtech innovations have democratized access to institutional-grade alternatives. Today, accredited investors can build customizable portfolios that include:

Private Equity – Access to company ownership before IPOs

Private Credit – Direct lending opportunities with attractive yields

Real Estate Syndication – Fractional ownership in commercial properties

Infrastructure – Essential assets like data centers, renewable energy, and logistics

Digital Assets – Institutional-grade Bitcoin and crypto exposure

Art and Collectibles – Alternative stores of value with unique return profiles

Assets like essential infrastructure and real estate offer an additional bonus: many underlying contracts include inflation adjustment clauses. As consumer prices rise, your income streams adjust upward. It's a natural hedge baked right into the investment.

Implementing the 40/30/30 Model: A Practical Approach

Knowing the theory is one thing. Executing it is another. Here's how to put the 40/30/30 framework into action.

Step 1: Audit Your Current Allocation

Before making changes, understand where you stand. What's your current split between equities, fixed income, and alternatives? Most investors are surprised to find they're far more concentrated in public markets than they realized.

Step 2: Define Your Alternative Functions

Don't just throw money at alternatives randomly. Decide how much of your 30% allocation should go toward downside protection, uncorrelated returns, and upside capture. Your mix depends on your risk tolerance, time horizon, and current market outlook.

Step 3: Select Quality Managers and Vehicles

Not all alternative investments are created equal. Manager selection matters enormously in private markets. Look for track records, alignment of interests (do they invest alongside you?), and transparency in reporting.

Step 4: Plan for Liquidity

Alternatives often come with lockup periods. Make sure your overall portfolio has enough liquidity to meet near-term needs without forcing you to sell illiquid positions at inopportune times.

Step 5: Rebalance Dynamically

The 40/30/30 model isn't set-and-forget. Market conditions change. Your alternative allocation should adapt accordingly. In periods of high uncertainty, you might tilt toward downside protection. In recovery phases, lean into upside capture strategies.

Why This Matters in 2026

We're operating in an environment marked by:

Persistent inflation concerns that erode purchasing power

Interest rate uncertainty that challenges traditional bond portfolios

Geopolitical tensions that create sudden market dislocations

Technological disruption that reshapes entire industries

The 40/30/30 model addresses all of these challenges by building resilience into the portfolio structure itself. It's not about predicting what happens next: it's about being prepared for multiple scenarios.

Major institutional investors have already made this shift. Pension funds, endowments, and family offices have been moving toward higher alternative allocations for years. The difference now? Accredited investors can access similar strategies.

Building Your 40/30/30 Portfolio

The 40/30/30 portfolio model represents a genuine evolution in investment thinking. It acknowledges the limitations of traditional allocations while capitalizing on the expanded opportunity set available to today's accredited investors.

At Mogul Strategies, we specialize in blending traditional assets with innovative digital strategies to build portfolios designed for long-term wealth preservation and growth. Whether you're looking to integrate institutional-grade alternatives, explore private equity opportunities, or add strategic digital asset exposure, we're here to help you navigate the path forward.

The market has changed. Your portfolio should too.

Comments