The Institutional Investor's Guide to the 40/30/30 Portfolio Model in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 21

- 5 min read

Let's be honest: if you're still running a traditional 60/40 portfolio in 2026, you're essentially driving a car with a 1980s GPS. It might get you somewhere, but you're missing a lot of better routes.

The investment landscape has fundamentally shifted. Stocks and bonds aren't playing by the old rules anymore, and institutional investors are taking notice. Enter the 40/30/30 portfolio model: a framework that's gaining serious traction among sophisticated investors looking for better risk-adjusted returns in today's market environment.

Here's what you need to know.

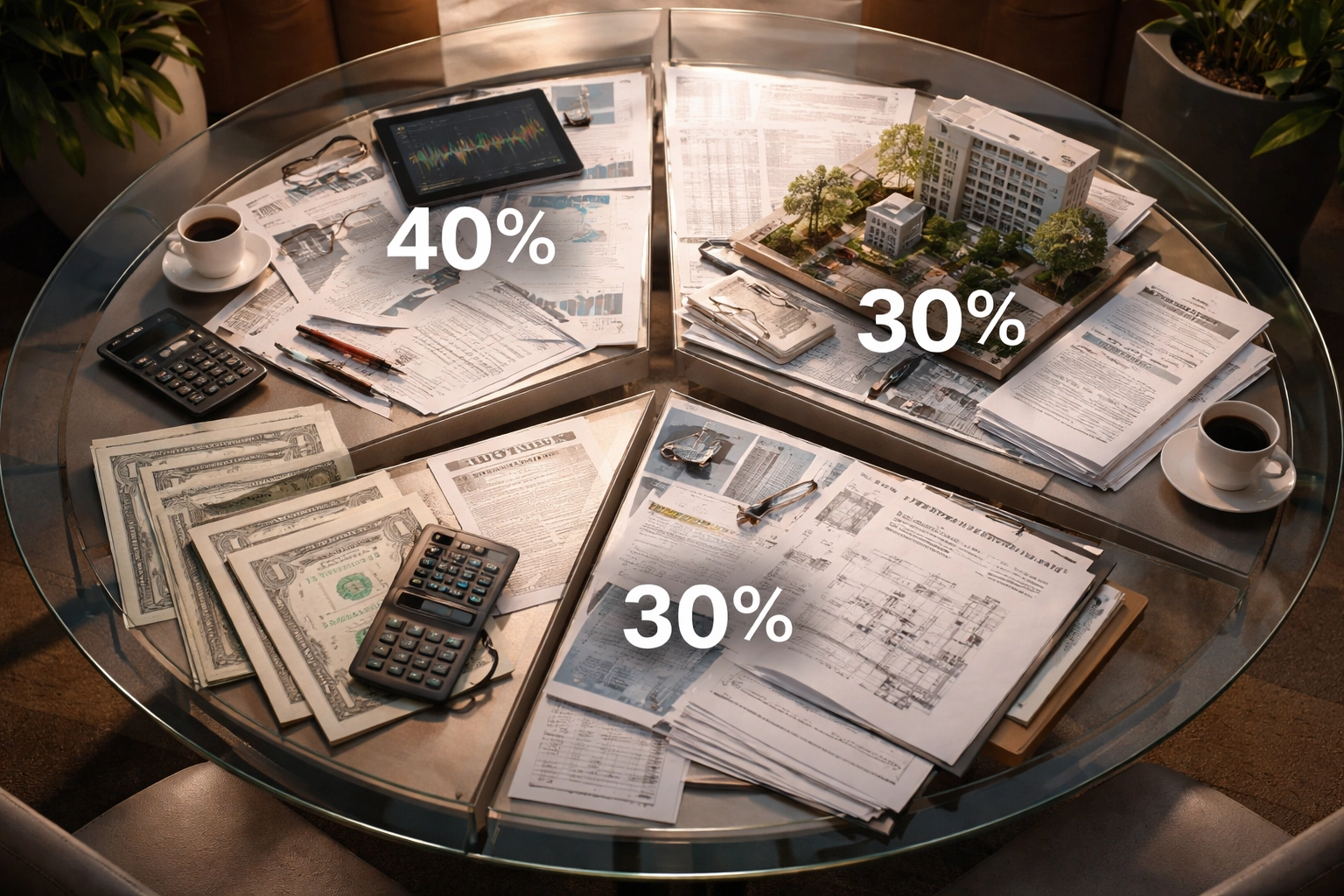

What Exactly Is the 40/30/30 Model?

The 40/30/30 portfolio model breaks down like this:

40% public equities

30% fixed income

30% alternative investments

That's it. Simple on the surface, but the implications are significant. You're essentially trimming your equity exposure by 20 percentage points compared to the traditional 60/40 and redirecting that capital into alternatives: think private equity, real estate, infrastructure, and private credit.

The goal isn't to chase higher returns at any cost. It's about building a portfolio that actually behaves the way diversified portfolios are supposed to behave.

Why the 60/40 Model Is Showing Its Age

For decades, the 60/40 split between stocks and bonds was the gold standard. The logic was straightforward: when stocks zigged, bonds zagged. You got growth from equities and stability from fixed income. Beautiful, right?

Here's the problem: that relationship has broken down.

We're living in an era of "higher for longer" interest rates, persistent inflation pressures, and geopolitical tensions that would make a cold war historian nervous. Stocks and bonds are increasingly moving in tandem rather than offsetting each other. When both asset classes decline simultaneously: as we saw during several periods in the early 2020s: the entire premise of the 60/40 model falls apart.

Nearly 8 in 10 U.S. institutional investors foresee a market correction in 2026. They're not sitting around hoping the old playbook still works. They're adapting.

The Numbers Don't Lie: Performance Advantages

Let's talk concrete data, because that's what matters when you're managing serious capital.

J.P. Morgan's research found that adding a 25% allocation to alternatives can improve traditional 60/40 returns by 60 basis points. That might sound modest until you realize it represents an 8.5% improvement on the projected 7% baseline return. Over time, that compounds into real money.

But here's where it gets interesting. KKR's analysis showed the 40/30/30 model outperformed the 60/40 approach by 2.6 percentage points between June 2020 and June 2022: a particularly volatile period that stress-tested both approaches.

Even more telling? The Sharpe ratio: which measures risk-adjusted returns: improved from 0.41 to 0.85. That's more than double the risk-adjusted performance. You're not just making more money; you're making it more efficiently relative to the risk you're taking.

Breaking Down the 30% Alternatives Allocation

Not all alternative investments are created equal, and how you structure that 30% matters enormously.

KKR recommends a straightforward three-way split for institutional portfolios:

Asset Class | Allocation |

Real Estate | 10% |

Infrastructure | 10% |

Private Credit | 10% |

This approach balances income generation, inflation protection, and diversification benefits across different economic cycles.

For investors who need to maintain more liquidity, there's a modified approach worth considering:

10% private equity

10% private credit

5% real estate

5% infrastructure

The key is matching your alternatives allocation to your actual liquidity needs and investment horizon. There's no one-size-fits-all answer here.

Why Alternatives Are Earning Their Seat at the Table

Let's break down what each alternative asset class brings to the party.

Private Credit: The Star Performer

Private credit has emerged as a particularly compelling diversifier. Newly issued junior debt and asset-based securities are expected to deliver 13.5-14.5% annualized returns over the next three years. That's serious yield in an environment where traditional fixed income is struggling to keep pace with inflation.

About 45% of institutional investors are currently increasing their allocations to private debt. They're not doing it because it's trendy: they're doing it because the risk-reward profile makes sense.

Real Estate and Infrastructure: Built-In Inflation Protection

Both real estate and infrastructure investments often come with inflation adjustment clauses baked directly into contracts. When inflation rises, your income streams rise with it. That's a feature, not a bug.

These asset classes also tend to show lower correlation with public markets, meaning they can provide genuine diversification benefits when you need them most: during market stress.

Private Equity: Growth Engine

While private equity requires longer lock-up periods and carries higher risk, it also offers access to growth opportunities unavailable in public markets. About 34% of institutional investors are increasing their private equity exposure, seeking alpha that's increasingly difficult to find in efficient public markets.

What Institutional Investors Are Actually Doing in 2026

Here's an interesting wrinkle: while the 40/30/30 model is gaining attention, institutional investor adoption shows some variation in implementation.

Over 71% of institutional investors believe that a 60:20:20 mix (equities: fixed income: alternatives) will outperform the traditional 60/40 approach. That's a slightly more conservative step toward alternatives than the full 40/30/30, but it still represents a meaningful shift in thinking.

The takeaway? There's broad consensus that alternatives deserve a larger role. The exact allocation depends on each institution's specific circumstances, risk tolerance, and liquidity requirements.

Implementation Considerations

Moving from theory to practice requires careful planning. Here are the key factors to consider:

Liquidity Management Alternative investments typically come with longer lock-up periods. Make sure your portfolio can handle reduced liquidity without forcing you to sell at inopportune times.

Manager Selection Unlike index funds, alternatives require active management. The spread between top-quartile and bottom-quartile managers is significant. Choose carefully.

Due Diligence Alternative investments often have complex fee structures and risk profiles. Understand what you're buying before you commit capital.

Rebalancing Strategy With illiquid alternatives in the mix, traditional rebalancing becomes more challenging. Build flexibility into your allocation targets.

The Bottom Line

The 40/30/30 portfolio model isn't a magic bullet. No allocation strategy is. But it represents a thoughtful response to genuine changes in how markets behave.

When stocks and bonds move together, the old diversification playbook stops working. When inflation erodes purchasing power, you need assets with built-in protection. When public market returns compress, you need access to alternative sources of alpha.

The institutional investors who are thriving in 2026 aren't the ones clinging to strategies designed for a different era. They're the ones adapting their approaches to match current realities.

At Mogul Strategies, we specialize in helping sophisticated investors navigate exactly these kinds of strategic decisions: blending traditional assets with innovative approaches to build portfolios designed for today's market environment.

The question isn't whether alternatives deserve a place in institutional portfolios. The data has settled that debate. The question is how to implement that allocation effectively for your specific situation.

That's where the real work begins.

Comments