The Proven 40/30/30 Framework: How Institutional Investors Are Building Diversified Portfolios in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 18

- 5 min read

The 60/40 portfolio had a good run. For decades, it was the gold standard of diversification, 60% stocks for growth, 40% bonds for stability. Simple. Elegant. Reliable.

Until it wasn't.

In 2026, institutional investors have largely moved on. They're now building portfolios around a different framework: the 40/30/30 model. And if you're an accredited investor still clinging to the old playbook, it might be time to catch up.

Let's break down what this framework looks like, why it works, and how you can apply it to your own portfolio strategy.

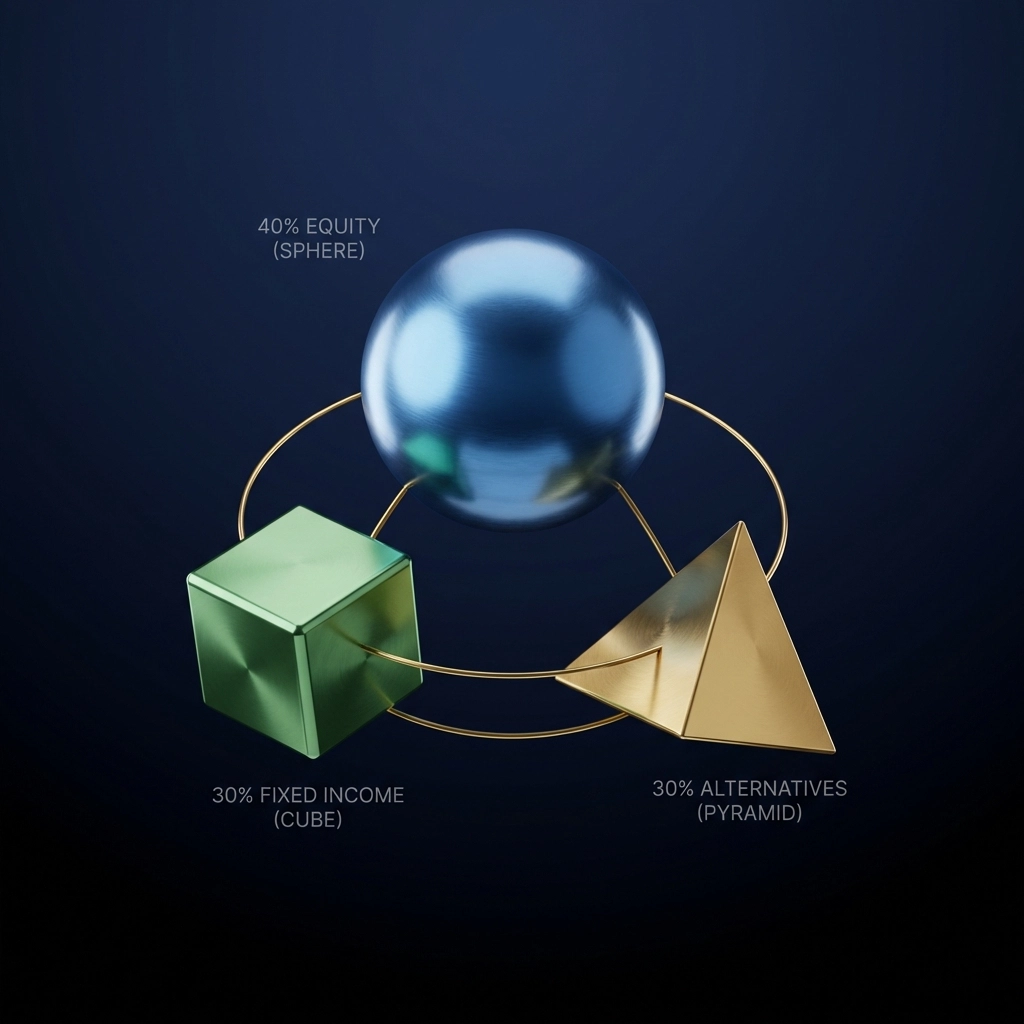

What Is the 40/30/30 Framework?

The 40/30/30 framework is straightforward:

40% in public equities (stocks)

30% in fixed income (bonds and similar instruments)

30% in alternative investments (private equity, real estate, infrastructure, hedge funds, and yes, digital assets like Bitcoin)

This isn't some fringe theory. Major institutions, including endowments, pension funds, and family offices, have been allocating 40% or more to alternatives for years. The 40/30/30 model simply formalizes what the smart money has been doing all along.

The goal? Build a portfolio that doesn't fall apart when markets get rough.

Why the Traditional 60/40 Model Stopped Working

Here's the uncomfortable truth about the 60/40 portfolio: it was never really diversified.

During normal market conditions, stocks and bonds moved in opposite directions. Stocks went up, bonds stayed steady. Stocks dropped, bonds provided a cushion. It worked beautifully, until it didn't.

In recent years, we've seen:

Persistently high interest rates that crushed bond prices

Volatile inflation that eroded purchasing power across asset classes

Geopolitical tensions that sent shockwaves through global markets

During the 2008 financial crisis and the 2020 pandemic crash, the 60/40 portfolio lost over 30%. That's not diversification. That's correlation in disguise.

Research shows that during major downturns, the 60/40 portfolio exhibited a correlation close to 1 with equities. In plain English: when stocks crashed, the "diversified" portfolio crashed right alongside them.

The 40/30/30 framework addresses this fundamental flaw by introducing assets that genuinely behave differently from public markets.

The Numbers Behind the Framework

Let's talk performance. Because at the end of the day, frameworks only matter if they deliver results.

According to research from J.P. Morgan and KKR, the 40/30/30 approach offers:

For institutional investors managing billions, these improvements translate to massive dollar amounts. For individual accredited investors, they can mean the difference between a comfortable retirement and an exceptional one.

How Institutions Actually Build These Portfolios

Here's where things get interesting. Institutional investors don't just throw 30% into "alternatives" and call it a day. They're strategic about it.

The Functional Allocation Approach

Rather than treating alternatives as one big bucket, sophisticated investors classify them by their role in the portfolio:

1. Downside Protection Strategies These are the assets designed to hold steady (or even gain value) when markets tank. Think certain hedge fund strategies, managed futures, or gold allocations.

2. Uncorrelated Return Generators These assets provide returns that don't move in lockstep with stocks or bonds. Private credit, certain real estate investments, and infrastructure projects fall into this category. They create stability through genuine diversification.

3. Upside Capture Opportunities These are growth-oriented alternatives, private equity, venture capital, and increasingly, digital assets like Bitcoin. They aim to deliver outsized returns during favorable market conditions.

The key insight? Not all alternatives are created equal. A well-constructed 30% alternatives allocation might include pieces from each of these three categories, balanced according to your specific goals and risk tolerance.

Dynamic Rebalancing

Institutional investors don't set their allocations once and forget about them. They employ active, centralized allocation that adjusts to real-time market changes and macroeconomic conditions.

When inflation spikes, they might increase exposure to real assets with built-in inflation protection. When credit spreads widen, they might opportunistically add private credit. When equity valuations look stretched, they might dial back public market exposure.

This dynamic approach requires expertise, data, and discipline, but it's a core reason why institutional portfolios tend to weather storms better than static allocations.

Strategic Asset Selection: What Goes in the 30%

Let's get specific about what institutional investors are actually putting in their alternatives bucket in 2026.

Real Estate and Infrastructure

These assets offer something unique: inflation adjustment clauses built directly into their contracts. When consumer prices rise, rental income and infrastructure fees often rise with them. That provides a natural hedge that bonds simply can't offer.

Private Equity and Private Credit

Private markets have delivered premium returns compared to public markets for decades. Yes, they come with less liquidity. But for investors with longer time horizons, that illiquidity premium can significantly boost overall portfolio performance.

Digital Assets

Bitcoin and other digital assets have earned a seat at the institutional table. The volatility concerns are real, but so is the diversification benefit. Properly sized (typically 1-5% of the overall portfolio), digital assets can improve risk-adjusted returns without introducing unacceptable volatility.

Hedge Fund Strategies

Not all hedge funds are created equal, but the right strategies: particularly those focused on market-neutral or macro approaches: can provide genuine downside protection during equity market drawdowns.

The Democratization of Institutional Strategies

Here's the good news: you don't need a billion-dollar endowment to access these strategies anymore.

What once required $500,000 minimum investments is now available to millions of investors. Private market platforms, interval funds, and specialized asset managers have opened doors that were firmly closed just a decade ago.

At Mogul Strategies, we specialize in helping accredited investors build portfolios that blend traditional assets with innovative digital strategies: the same approach that institutional investors have used for years.

Putting It Into Practice

If you're considering shifting toward a 40/30/30 framework, here are some practical steps:

1. Audit your current allocation. Most investors are surprised to find they're more concentrated in public equities than they realized.

2. Define your objectives. Are you focused on downside protection, return enhancement, or both? Your answer shapes which alternative strategies make sense.

3. Start with accessible alternatives. REITs, interval funds, and regulated digital asset products can provide alternatives exposure without complex structures.

4. Work with specialists. Building a truly diversified portfolio requires expertise across multiple asset classes. This isn't a DIY project for most investors.

5. Think long-term. Many alternative investments require patience. The benefits compound over years, not months.

The Bottom Line

The 40/30/30 framework isn't revolutionary: it's simply what sophisticated institutional investors have been doing for decades, now formalized and accessible to a broader audience.

The traditional 60/40 portfolio served its purpose in a different era. But in 2026, with elevated rates, persistent inflation concerns, and ongoing geopolitical uncertainty, genuine diversification requires genuine alternatives.

The question isn't whether the 60/40 model is dead. It's whether you're ready to build something better.

Comments