The Proven 40/30/30 Portfolio Framework for Institutional Investors (Bitcoin Integration Included)

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Feb 1

- 5 min read

The traditional 60/40 portfolio split between stocks and bonds worked great for decades. But if you're managing institutional capital in 2026, you already know that framework is showing its age. When both equities and fixed income can tank simultaneously (hello, 2022), you need something more robust.

That's where the 40/30/30 framework comes in, and yes, we're going to talk about how Bitcoin fits into this picture for institutions that are ready to think beyond traditional alternatives.

Why the 60/40 Portfolio Isn't Cutting It Anymore

Let's be honest. The classic 60/40 portfolio was built for a different era: one with higher interest rates, lower correlations between asset classes, and predictable inflation. Today's institutional investors face a different reality:

Bond yields that barely keep pace with inflation

Stock-bond correlations that spike exactly when you need diversification most

Increased volatility across traditional markets

Limited alpha generation from conventional strategies

Institutions have known this for years. That's why many endowments and pension funds already allocate 40% or more to alternative investments. The 40/30/30 framework basically takes that institutional wisdom and makes it more accessible.

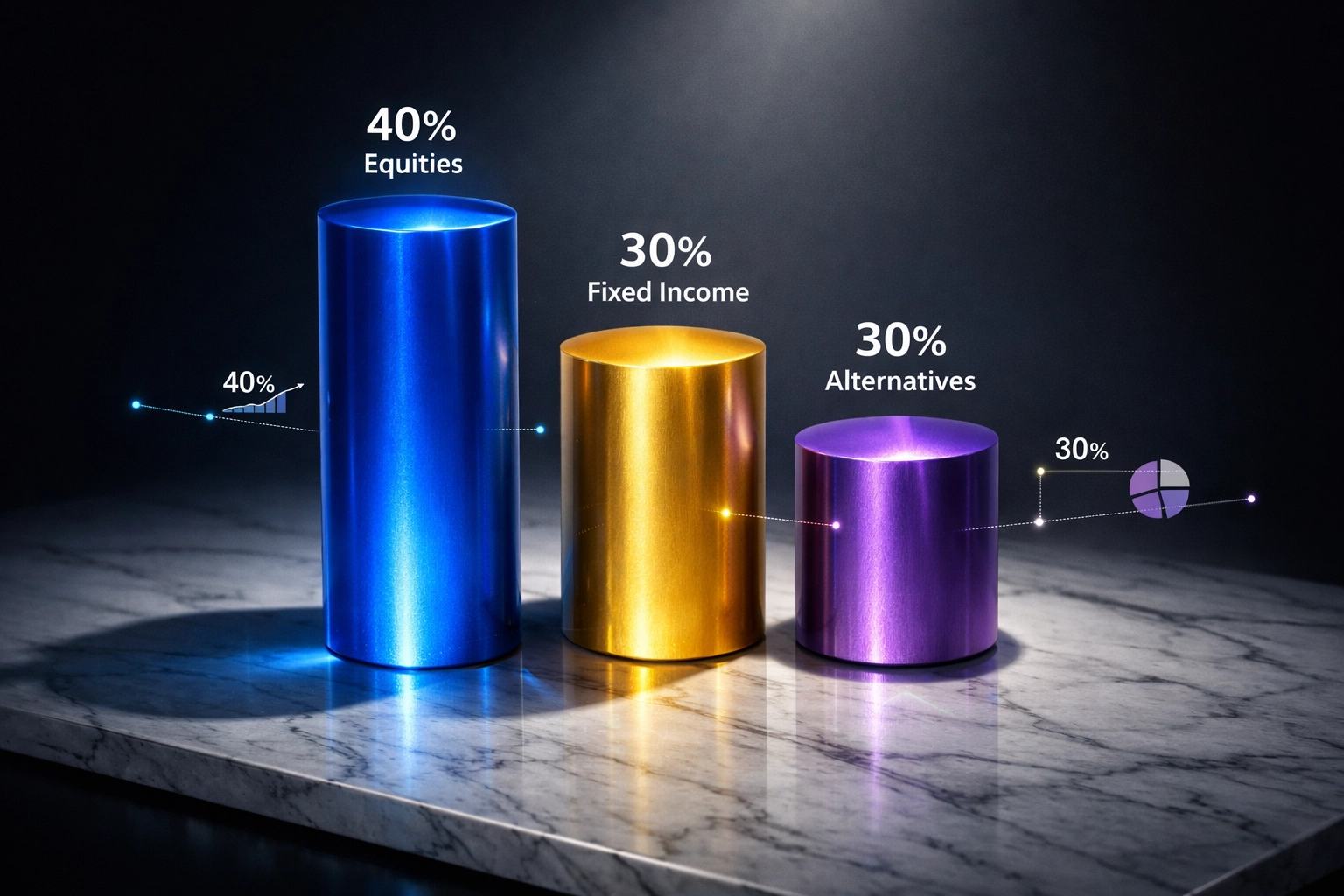

Breaking Down the 40/30/30 Framework

Here's the basic structure:

40% Public Equities – Your growth engine. This includes domestic and international stocks, with exposure across market caps and sectors. Think blue-chip companies, emerging markets, and sector-specific plays.

30% Fixed Income – Your stability anchor. Government bonds, corporate debt, TIPS (Treasury Inflation-Protected Securities), and other fixed-income instruments that provide steady income and downside protection.

30% Alternative Investments – Your diversification powerhouse. This is where things get interesting. Private equity, real estate, infrastructure, commodities, hedge fund strategies: and yes, for forward-thinking institutions, Bitcoin and digital assets.

Research backs this up. J.P. Morgan found that adding a 25% allocation to alternatives can boost traditional portfolio returns by 60 basis points. That's an 8.5% improvement over the standard 60/40's projected 7% return. KKR's analysis went further, showing the 40/30/30 structure outperformed the 60/40 across every timeframe they studied.

The 40%: Public Equities Done Right

Your equity allocation shouldn't just be a total market index fund and call it a day. Institutional investors know that smart equity allocation means:

Geographic diversification across developed and emerging markets

Sector rotation based on economic cycles

Factor exposure (value, growth, momentum, quality)

Small-cap and mid-cap opportunities beyond large-cap stalwarts

The goal here is straightforward growth with manageable volatility. You're not trying to hit home runs: you're building a reliable foundation that compounds over time.

The 30%: Fixed Income as Your Ballast

In 2026, fixed income requires more sophistication than it did a decade ago. Your 30% allocation should include:

Core Holdings: Investment-grade corporate bonds and treasuries that provide stability and liquidity.

Inflation Protection: TIPS and other inflation-linked securities that adjust as consumer prices rise. With inflation remaining unpredictable, this isn't optional.

Credit Opportunities: High-quality corporate debt that offers yield pickup without excessive default risk.

The key is duration management. Longer-duration bonds are more sensitive to rate changes, while shorter-duration instruments offer less yield but greater stability. Your mix depends on your risk tolerance and interest rate outlook.

The 30%: Alternatives (Including Bitcoin) as Your Edge

This is where institutional investors separate themselves from retail portfolios. That 30% alternatives bucket can be split across multiple asset classes:

Traditional Alternatives

Private Equity (8-12%): Access to non-public companies with potentially higher returns than public markets. The illiquidity premium is real, and patient capital gets rewarded.

Real Estate (6-10%): Direct property investments, REITs, and real estate syndications. These provide cash flow, inflation hedging, and low correlation to equities.

Infrastructure (4-8%): Toll roads, utilities, renewable energy projects. These assets often have inflation-adjustment clauses built into contracts.

Commodities (2-5%): Gold, energy, agriculture. Natural hedges against specific economic scenarios.

Digital Assets: The Bitcoin Allocation

Here's where it gets interesting for 2026. Institutional-grade Bitcoin allocation isn't about speculation: it's about recognition that digital assets represent a genuinely uncorrelated asset class with specific portfolio benefits.

The Case for Institutional Bitcoin Exposure (2-5% of total portfolio):

Bitcoin has matured significantly. We now have regulated custody solutions, transparent ETFs, and institutional infrastructure that didn't exist years ago. For the alternatives bucket, a measured Bitcoin allocation provides:

True diversification: Bitcoin's correlation to traditional assets remains low over extended periods

Inflation hedge characteristics: Fixed supply makes it an interesting counterweight to fiat currency debasement

Growth potential: Still early in institutional adoption curve

Portfolio volatility management: Small allocations can actually reduce overall portfolio volatility when properly sized

The key word is "measured." We're talking 2-5% of your total portfolio, which means roughly 7-17% of your alternatives bucket. This isn't a casino bet: it's a calculated position in an emerging asset class that's reached institutional maturity.

Implementation Considerations for Bitcoin:

Use regulated custody solutions (Coinbase Prime, Fidelity Digital Assets, etc.)

Access through ETFs for simpler administration and reporting

Treat it as a long-term holding with 3-5 year minimum time horizons

Rebalance according to policy, not emotion

Ensure proper governance and risk management frameworks

Performance Reality Check

Let's talk numbers. Based on historical data and institutional research, a well-constructed 40/30/30 portfolio with Bitcoin integration has shown:

Enhanced risk-adjusted returns compared to 60/40

Lower drawdowns during equity market stress

Better inflation protection through real assets

Reduced correlation between portfolio components

More consistent income generation

The illiquidity premium from private assets contributes to alpha generation, while the diversification benefits reduce portfolio-wide volatility. Adding a small Bitcoin allocation can actually enhance Sharpe ratios when properly sized.

Risk Considerations You Can't Ignore

No framework is perfect. Here's what you need to watch:

Liquidity Management: With 30% in alternatives, you need strong liquidity planning. Not everything can be sold on demand.

Due Diligence Requirements: Alternatives demand deeper analysis than public securities. Manager selection matters enormously.

Fee Structures: Private investments often carry higher fees. Make sure the net returns justify the costs.

Operational Complexity: More asset classes mean more administration, reporting, and oversight.

Bitcoin Volatility: Even at small allocations, Bitcoin's price swings can affect portfolio dynamics. Proper position sizing is critical.

Regulatory Evolution: Digital asset regulations continue developing. Stay ahead of compliance requirements.

Making It Work for Your Institution

The 40/30/30 framework isn't one-size-fits-all. Your specific allocation depends on:

Investment time horizon

Liquidity needs

Risk tolerance

Access to quality alternative investments

Operational capabilities

Regulatory constraints

Some institutions might dial up the alternatives to 35% or 40%. Others might keep Bitcoin out entirely if their investment policy statement doesn't allow it yet. The framework is a starting point, not a straitjacket.

The Bottom Line

The 40/30/30 portfolio framework represents how sophisticated institutions are actually allocating capital today. It acknowledges that traditional 60/40 portfolios aren't optimized for current market realities.

By reducing equity concentration, maintaining fixed income ballast, and thoughtfully deploying alternatives: including measured Bitcoin exposure for qualified institutions: you build portfolios that are more resilient across economic environments.

The data supports it. The institutions with the longest track records are doing it. The question isn't whether the 40/30/30 framework makes sense: it's how you implement it for your specific situation.

If you're managing institutional capital and want to explore how this framework could work for your portfolio, including the nuances of Bitcoin integration done right, let's talk. Because in 2026, staying with yesterday's portfolio construction isn't a conservative choice; it's an uncompensated risk.

Comments