The Accredited Investor's Guide to the 40/30/30 Diversification Model in 2026

- Technical Support

.png/v1/fill/w_320,h_320/file.jpg)

- Jan 29

- 5 min read

If you've been in the investment game for a while, you've probably heard about the classic 60/40 portfolio. It was the gold standard for decades: 60% equities, 40% bonds, and call it a day. But here's the thing: that playbook doesn't work the way it used to.

Market dynamics have shifted. The correlation between stocks and bonds has changed. And accredited investors like you are looking for something that actually delivers in today's environment.

Enter the 40/30/30 model.

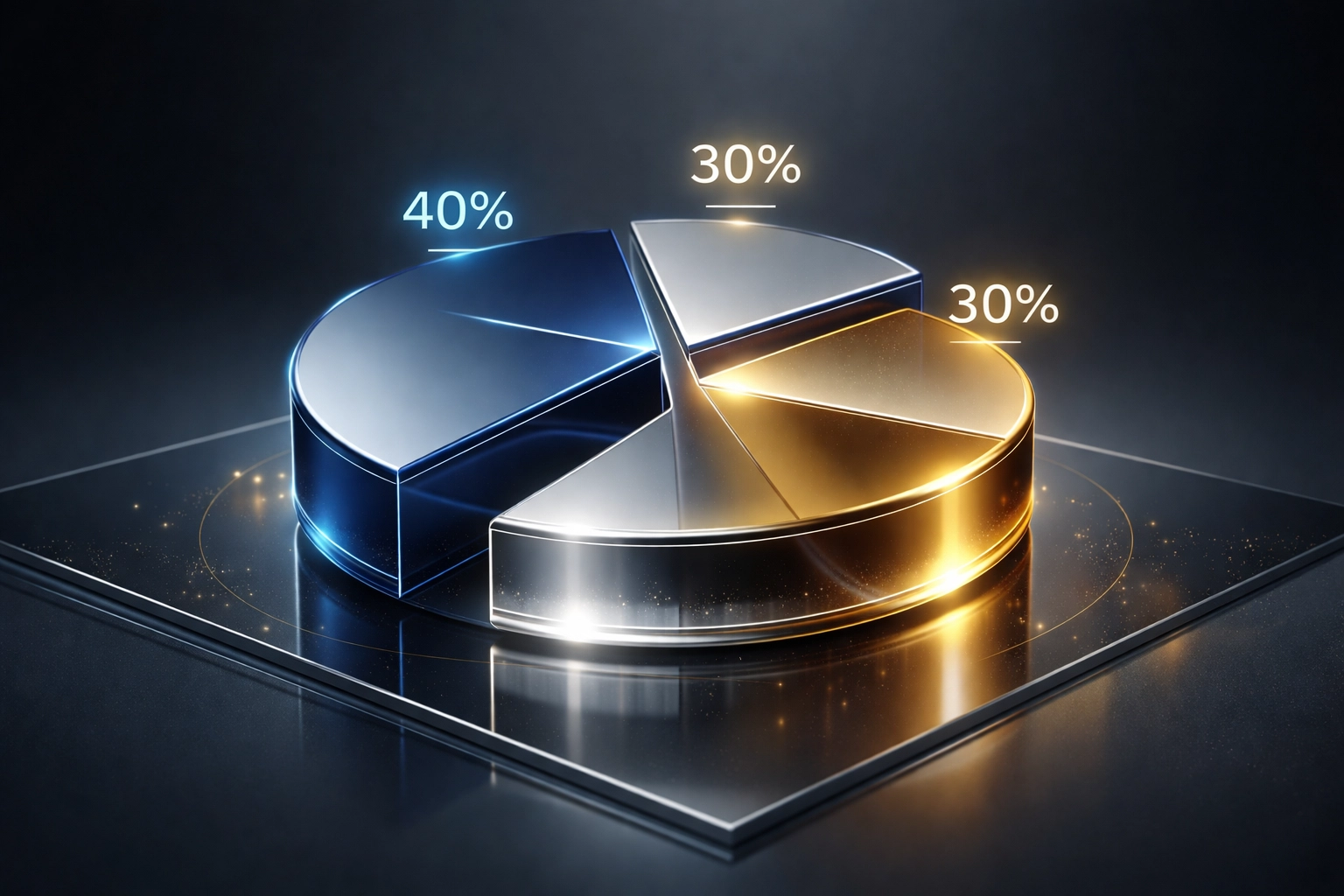

What Exactly Is the 40/30/30 Portfolio?

Let's break it down simply:

40% Equities – Your growth engine

30% Fixed Income – Your stability anchor

30% Alternative Investments – Your diversification powerhouse

This isn't just a minor tweak to the old formula. It's a fundamental rethinking of how sophisticated portfolios should be constructed in 2026 and beyond.

The 30% allocation to alternatives is the game-changer here. We're talking about assets like private equity, real estate syndications, hedge funds, infrastructure, and yes: institutional-grade digital assets like Bitcoin.

Why the 60/40 Model Stopped Working

For decades, the 60/40 portfolio delivered. Stocks provided growth, bonds cushioned the blows during downturns, and everyone was relatively happy.

But something changed.

Stocks and bonds started moving together. In recent years, when equities dropped, bonds didn't provide the protection investors expected. During both upswings and downturns, these asset classes moved in tandem: completely undermining the diversification benefit you were counting on.

Bond yields couldn't keep up. With interest rate fluctuations and compressed yields, fixed income simply doesn't offer the returns or downside protection it once did.

Concentration risk became real. A 60/40 portfolio now shows a correlation close to 1 with the equity market. Translation? When stocks tank, your "diversified" portfolio tanks with them. We've seen losses exceeding 30% during crises: not exactly what you signed up for.

The bottom line: the 60/40 model wasn't designed for today's macroeconomic reality.

The Numbers Don't Lie: 40/30/30 Performance

Here's where things get interesting for the data-driven investors out there.

Research from major institutions has validated what forward-thinking fund managers have suspected for years:

40% improvement in Sharpe ratio – The 40/30/30 strategy demonstrates significantly better risk-adjusted returns compared to the traditional 60/40 approach

Higher returns with lower volatility – Historical analysis over 25 years shows the model delivers more upside while smoothing out the ride

Institutional backing – J.P. Morgan research found that a 25% allocation to alternatives can boost 60/40 returns by 60 basis points (an 8.5% improvement). KKR's analysis showed 40/30/30 outperformed 60/40 across all studied timeframes

These aren't marginal improvements. For accredited investors managing substantial capital, even small percentage gains compound into serious wealth over time.

Understanding the Alternatives Sleeve

Now, here's where many investors get it wrong. They hear "alternative investments" and think it's all one thing. It's not.

The smart approach: used by institutional players like Candriam: is to classify alternatives by their functional role in your portfolio:

Downside Protection

These are assets designed to hedge against equity losses. Think managed futures, certain hedge fund strategies, or gold allocations. When markets panic, these should hold steady or even appreciate.

Uncorrelated Returns

Strategies that perform independently of traditional markets. This includes certain private credit investments, market-neutral hedge funds, and some real asset classes. The goal here is genuine diversification: returns that don't care what the S&P 500 is doing.

Upside Potential

Growth-oriented alternatives that capture opportunities traditional assets can't reach. Private equity, venture capital exposure, real estate syndications, and institutional-grade crypto positions fall into this bucket.

The key insight? You don't just dump 30% into "alternatives" and hope for the best. You build that sleeve with intention, balancing these three functions based on your goals and the current economic regime.

Implementing 40/30/30 as an Accredited Investor

Let's get practical. How do you actually put this to work?

Start with accessibility. The good news: alternatives are more accessible than ever. Previously, accessing private markets required minimum investments exceeding $500,000. Today, accredited investors can build meaningful alternative exposure with lower entry points through syndications, funds, and institutional platforms.

Balance liquidity thoughtfully. The 40/30/30 model maintains adequate liquidity through your public equity and fixed income allocations. This gives you room to hold less liquid private assets: infrastructure, real estate, private credit: that reward patient capital with consistent income streams and potential appreciation.

Consider inflation resilience. Alternative asset classes like essential infrastructure and real estate often include inflation adjustment clauses in their underlying contracts. As consumer prices rise, your income streams can rise with them. That's a natural hedge your bond allocation simply can't provide.

Stay dynamic. The best 40/30/30 implementations aren't static. Active management that responds to macroeconomic changes: adjusting the portfolio's composition based on economic regime: can further enhance results. This is where working with an experienced fund manager pays dividends.

The Role of Digital Assets in Modern Alternatives

We'd be remiss not to address the elephant in the room: Bitcoin and institutional-grade crypto.

For accredited investors in 2026, thoughtfully integrated digital asset exposure has become part of sophisticated alternative allocations. We're not talking about speculative meme coins. We're talking about Bitcoin as a potential inflation hedge and portfolio diversifier, held through institutional custody solutions with proper risk management.

Within the alternatives sleeve, digital assets can serve multiple functions: uncorrelated returns during certain market conditions, upside potential during adoption cycles, and increasingly, a store of value role that complements traditional hard assets.

The key is integration, not speculation. Position sizing, custody solutions, and correlation analysis all matter when incorporating crypto into a 40/30/30 framework.

Why 2026 Is the Right Time

The macroeconomic environment we're operating in: characterized by regime change, persistent inflation concerns, and evolving correlation patterns: makes the case for 40/30/30 stronger than ever.

Institutional investors have been moving this direction for years. Pension funds, endowments, and family offices have long maintained significant alternative allocations. What's changed is accessibility. Accredited investors can now build portfolios that rival institutional sophistication.

Within the alternatives space, private credit has emerged as particularly compelling given recent market conditions. Real estate syndications continue offering tax-advantaged income streams. And infrastructure investments provide the kind of stable, inflation-linked cash flows that help you sleep at night.

Making It Work for You

The 40/30/30 model isn't a one-size-fits-all prescription. It's a framework: a starting point for building a portfolio that actually addresses contemporary market realities.

Your specific allocation will depend on your liquidity needs, tax situation, risk tolerance, and investment timeline. The 30% alternatives sleeve might lean heavier toward real estate if you value income. Or it might emphasize private equity if you're optimizing for long-term growth.

What matters is the principle: meaningful diversification requires moving beyond the stocks-and-bonds binary. The traditional 60/40 served its purpose for a different era. The 40/30/30 model offers a path forward that balances historical wisdom with modern reality.

At Mogul Strategies, we specialize in helping accredited investors implement sophisticated diversification strategies that blend traditional assets with innovative opportunities. Whether you're exploring your first alternative allocation or optimizing an existing portfolio, the 40/30/30 framework provides a foundation worth considering.

The markets have evolved. Your portfolio strategy should too.

Comments